nueva página del texto (beta)

nueva página del texto (beta) Inglés (pdf)

Inglés (pdf)

Artículo en XML

Artículo en XML Referencias del artículo

Referencias del artículo

Enviar artículo por email

Enviar artículo por email Citado por SciELO

Citado por SciELO  Similares en

SciELO

Similares en

SciELO

Permalink

Permalink1. Introduction

An important resurgence of Microfinance Institutions (MFIs) took place in the 70’s when initially they were constituted as non-profit NGOs1, though the first antecedents are given since the 19th century in Europe (Germany).2 The MFIs mainly focus on providing financial services to the population that does not have access to conventional bank credit for lack of real collateral. MFIs face, continuously, two main objectives: 1) achieve financial sustainability, and 2) in-crease the number of clients. Currently, there are more than 2000 Microfinance Institutions (MFIs) in the world, with a total of 130 million clients and a Gross Loan Portfolio of 108 billion (USD)3.

On the other hand, the number of MFIs that are listed on stock exchanges is still small worldwide. However, they account for 16.8 % of the total number of clients since they have a high degree of concentration -in their respective markets where they operate. It is worth mentioning that MFIs seek in the stock market resources more efficiently (quickly and at a lower cost). The main question that arises is: if this objective can be achieved without being affected by the volatility from financial crises, which may discourage other MFIs from entering the stock market.

Due to the above concerns, Wagner and Winker (2011) and Di Della (2011) have studied the impact of financial crisis (for example, the sub-prime crisis, 2008) on the MFIs, particularly in periods of high volatility. However, the contagion in the volatility in the returns of the MFIs listed on stock markets has not yet been studied. In this sense, the goal of this paper is to analyze how volatility affects them. This will allows us to better understand the effects and consequences of high levels of volatility, which could be generated via global financial crises or high-volatility clusters. Thus, the main contribution of this research is to analyze, under a DCC-M-GARCH framework, how the contagion occurs in the volatilities of the returns of MFIs that are listed on stock exchanges in different emerging economies.

This paper analyzes five MFIs from three emerging economies: India, Indonesia and Mexico.4 Table 1 shows the studied MFIs and their characteristics such as number of clients, size of their portfolio and country of origin. In addition, for each MFI two reference variables are used in its corresponding stock market, and a global reference index -All Countries World index (ACWI). Table 2 describes each of the variables used (14 in total), it is shown the corresponding characteristics of: activity, currency in which they operate (in their respective stock market), and the period of analysis that comprises for each one of the MFIs, with daily frequency data.

Table 1 Microfinance Institutions (MFIs).

| MFI | Reporting Period | GrossLoan Portfolio (USD million) | No. of Active Borrowers (thousands) | Country |

|---|---|---|---|---|

| Gentera | 2015 | 1,317.76 | 2,861.72 | Mexico |

| Financiera Independencia | 2015 | 253.58 | 792.77 | Mexico |

| Bharat Financial Inclusion | 2014 | 671.79 | 5,325.24 | India |

| Limited: NSE and BSE | ||||

| Bank Rakyat Indonesia | 2012 | 10,897.40 | 12,918.43 | Indonesia |

Source: Own elaboration

Table 2 Description of Variables.

| Variables | Definition | Activity | Country | Currency | Starting date | Ending date |

|---|---|---|---|---|---|---|

| Gentera | Gentera | IMF | Mexico | MXN | 03-01-11 | 29-01-16 |

| IPC | Price Index and Quotations | Stock index | Mexico | MXN | 03-01-11 | 29-01-16 |

| MF | Mexican Found | Investment | EEUU | USD | 03-01-11 | 29-01-16 |

| ACWI | All Country World Index | Index | World | USD | 10-07-12 | 29-01-16 |

| FI | Financiera Independencia | IMF | México | MXN | 03-01-11 | 29-01-16 |

| BFIL_NSE | Bharat Financial Inclusion Limited NSE | IMF | India | INR | 03-01-11 | 29-01-16 |

| N50 | Nifty 50 | Stock index | India | INR | 03-01-11 | 29-01-16 |

| iI50 | ishares India 50 | Stock index | India | INR | 03-01-11 | 29-01-16 |

| BFIL_BSE | Bharat Financial Inclusion Limited BSE | IMF | India | INR | 03-01-11 | 29-01-16 |

| BD&MFG | BOMBAY DYEING & MFG.CO LTD | Textil | India | INR | 03-01-11 | 29-01-16 |

| BRFL | Bombay Rayon Fashion Limited | Textil | India | INR | 03-01-11 | 29-01-16 |

| BRI | Bank Rakyat Indonesia | Bank | Indonesia | IDR | 04-03-13 | 29-01-16 |

| JII | Jakarta Islamic Index | Stock index | Indonesia | IDR | 04-03-13 | 29-01-16 |

| TLK | TLK PT Telekomunikasi Indonesia | Comunications | Indonesia | IDR | 04-03-13 | 29-01-16 |

Source: the data was obtained from Yahoo Finance.

It is important to point out that the period of analysis is not the same for all MFIs. The reason is that, on the one hand, this research seeks to obtain as many observations as possible with the aim of achieving more robust results and, on the other hand, it is understandable that the periods are not homogeneous since the MFIs began to operate in the stock market on different dates; see the last two columns of Table 2.

In what follows, a descriptive statistical analysis is carried out in Table 3, According to the fifth column, all the returns are leptokurtic. Moreover, none of the returns are normally distributed according to the Jarque-Bera test. In Table 4, the unit root test was performed on each variable, using the Dickey Fuller Augmented test, under the three specifications: intercept, trend and intercept, and none. The results show that there is no empirical evidence of an explosive behavior in the analyzed variables.

Table 3 Descriptive statistics (in the returns of the variables).

| Returns | Mean | Std. Dev. | Skewness | Kurtosis | J-B | Prob. |

|---|---|---|---|---|---|---|

| Gentera | 0.0004 | 0.02 | 0.2 | 7.0 | 850.1 | 0.000 |

| IPC | 0.0001 | 0.01 | -0.2 | 5.7 | 382.8 | 0.000 |

| MF | -0.0003 | 0.01 | -0.3 | 5.2 | 282.0 | 0.000 |

| ACWI | 0.0002 | 0.01 | -0.5 | 5.8 | 337.0 | 0.000 |

| FI | -0.0008 | 0.02 | 0.3 | 9.7 | 2395.5* | 0.000 |

| BFIL_NSEN50 | 0.0005 | 0.04 | 0.4 | 6.8 | 786.2 | 0.000 |

| N50 | 0.0002 | 0.01 | -0.1 | 4.5 | 116.1 | 0.000 |

| iI50 | 0.0001 | 0.01 | -0.5 | 6.1 | 568.8 | 0.000 |

| BFIL_BSE | 0.0005 | 0.04 | 0.5 | 7.0 | 942.7 | 0.000 |

| BD&MFG | -0.0007 | 0.04 | -7.9 | 181.6* | 1755490.3* | 0.000 |

| BRFL | 0.0001 | 0.02 | 0.5 | 16.5 | 10043.1* | 0.000 |

| BRI | 0.0006 | 0.02 | 0.3 | 5.7 | 211.5 | 0.000 |

| JII | 0.0000 | 0.01 | 0.1 | 6.2 | 289.5 | 0.000 |

| TLK | 0.0003 | 0.02 | -0.1 | 5.9 | 240.2 | 0.000 |

Some results obtained, marked with the symbol “ * “ may seem to be erroneous; however, its result is due to values of high percentage variation of some observations, within the period of analysis.

Source: own elaboration with data from Yahoo Finance. The results were obtained using software EViews 7

Table 4 Results from Augmented Dickey-Fuller test (in the returns of the variables).

| Intercept | Trend and Intercept | None | ||||

|---|---|---|---|---|---|---|

| Variable | t-Statistic* | Prob. | t-Statistic** | Prob. | t-Statistic*** | Prob. |

| Gentera | -35.48 | 0.000 | -35.51 | 0.000 | -35.48 | 0.000 |

| IPC | -34.13 | 0.000 | -34.12 | 0.000 | -34.14 | 0.000 |

| MF | -21.67 | 0.000 | -21.70 | 0.000 | -21.66 | 0.000 |

| ACWI | -25.02 | 0.000 | -25.12 | 0.000 | -25.00 | 0.000 |

| FI | -35.17 | 0.000 | -35.17 | 0.000 | -35.13 | 0.000 |

| BFIL_NSE | -29.03 | 0.000 | -29.13 | 0.000 | -29.04 | 0.000 |

| N50 | -33.10 | 0.000 | -33.10 | 0.000 | -33.10 | 0.000 |

| iI50 | -31.48 | 0.000 | -31.51 | 0.000 | -31.49 | 0.000 |

| BFIL_BSE | -29.94 | 0.000 | -30.03 | 0.000 | -29.95 | 0.000 |

| BD&MFG | -34.07 | 0.000 | -34.06 | 0.000 | -34.07 | 0.000 |

| BRFL | -29.22 | 0.000 | -29.20 | 0.000 | -29.23 | 0.000 |

| BRI | -23.77 | 0.000 | -23.75 | 0.000 | -23.77 | 0.000 |

| JII | -18.50 | 0.000 | -18.49 | 0.000 | -18.52 | 0.000 |

| TLK | -25.47 | 0.000 | -25.46 | 0.000 | -25.48 | 0.000 |

Source: own elaboration with data from Yahoo Finance. The results were obtained by using software EViews 7.

In order to detect whether there are long-term memory effects in the returns of each variable, Hurst exponent is calculated. The latter is a useful indicator to examine whether returns have long-term memory -a characteristic useful to forecast future values. It is worth mentioning that Hurst’s exponent can be equal to 0.5 (without long-term memory), greater than 0.5 (long-term memory), and less than 0.5 (mean reversion). It is also important to notice that long-term memory violates the Efficient Market Hypothesis (EMH), established by Fama (1970). Moreover, this research computes an index of stock market liquidity5 in order to find some relationship between the effects of long memory and low stock market liquidity.

The obtained results, in relation to the Hurst exponent, show that Gentera and BRI do not present strong empirical evidence of long-term memory in their returns with Hurst exponents of 0.519 and 0.493, respectively.6 These results can be seen in the fourth column (in descending order) of Table 5. With respect to the obtained results in the liquidity index, see the sixth column (in ascending order) of Table 5, the MFIs that appear with less liquidity are FI and BRI with an index of 81.6 and 90.9, respectively.

Based on the previous results, there is not a pattern in the behavior between long-term memory and low market liquidity (as would be expected at first). However, we can highlight the case of FI with long memory and low liquidity, 0.56, 81.6 %, respectively. In contrast, Gentera shows an acceptable liquidity of 98 % and a Hurst exponent of 0.519. Notice also that BFIL_NSE and BFIL_BSE provide empirical evidence of long memory in its returns but with high levels of stock market liquidity -see columns fifth and seventh of Table 5.

Table 5 Hurst exponent and liquidity index (li).

| Variable returns |

Hurst/Exp. | Liquidity* index (li) |

Variable returns |

Hurst/Exp. Ranked |

Variable returns |

(li) renked |

|---|---|---|---|---|---|---|

| Gentera* | 0.519 | 98% | BFIL_NSE* | 0.586 | FI* | 81.60% |

| IPC | 0.505 | 100% | BFIL_NSE* | 0.586 | BRI* | 90.90% |

| MF | 0.561 | 97.50% | MF | 0.561 | BRFL | 97.40% |

| ACWI | 0.54 | 100% | FI* | 0.56 | MF | 97.50% |

| FI* | 0.56 | 81.60% | N50 | 0.549 | Gentera* | 98% |

| BFIL_NSE* | 0.586 | 99.30% | iI50 | 0.545 | TLK | 99.25% |

| N50 | 0.549 | 99.40% | ACWI | 0.54 | BFIL_NSE* | 99.30% |

| iI50 | 0.545 | 100% | BD&MFG | 0.534 | N50 | 99.40% |

| BFIL_BSE* | 0.586 | 99.50% | Gentera* | 0.519 | BD&MFG | 99.40% |

| BD&MFG | 0.534 | 99.40% | BRFL | 0.519 | JII | 99.40% |

| BRFL | 0.519 | 97.40% | IPC | 0.505 | BFIL_BSE* | 99.50% |

| BRI* | 0.493 | 90.90% | TLK | 0.495 | IPC | 100% |

| JII | 0.474 | 99.40% | BRI* | 0.493 | ACWI | 100% |

| TLK | 0.495 | 99.25% | JII | 0.474 | Ii50 | 100% |

Source: own elaboration. The results were obtained with the use of the R software, using the "pracma"library.

Each IMF is identified with the symbol “*”.

It is important to point out that not all the MFIs analyzed have had an acceptable long-term performance (in the period of analysis) in their accumulated returns. Only Gentera and BRI had a better performance than the local reference index in their respective markets, Mexico and Indonesia, respectively.

After the descriptive exploration of the variables, this research will be structured in the following way: section 2 provides a brief description of the M-GARCH model of Dynamic Conditional Correlation (DCC); section 3 presents the empirical findings for each specification of the MFIs (benchmark variables and a global index); finally, section 4 exposes the conclusion.

2. Dynamic Conditional Correlation (DCC)-M-GARCH

Recently, Bala and Takimoto (2017) analyze the effects of the dynamic correlation, during periods of financial crisis, by using a DCC-M-GARCH econometric approach. These authors found that the dispersion of volatilities among deve-loped markets is greater than in emerging markets. Previously, Mollah et al. (2014) study 63 countries during the period of the global financial crisis. These authors find -through the use of DCC- that contagion of volatility occurs in 46 out of 63 countries that is, in 73 % of the analyzed countries. Although the previous studies allow us to see some results related to the DCC-M-GARCH methodology in assessing the effects of contagion within emerging and developed markets, there is no recent literature that focuses on volatility contagion of returns of the MFIs listed on the stock market.7

On the other hand, Visconti (2009) argues that MFIs are affected in diffe-rent ways, depending on the country in which they operate and the degree to which these countries are integrated into the global economy. In addition, the author points out that MFIs operating in developing countries are less affected by financial crises due to close ties and constant monitoring of their clients. Moreover, Krauss and Walter (2008) applied a panel data approach (with fixed effects) in order to examine whether MFIs are a good option to reduce the volatility of an investment portfolio since their clients are mostly micro-entrepreneurs. In this regard, it is important to consider that the main disadvantage that MFIs face is that their clients do not have real guarantees. However, they do have the advantage of being able to maintain a continuous monitoring of their clients, which allows having a better quality in the portfolio of microcredits granted.

2.1 Generalized Autoregressive Conditional Heteroscedastic model

In this subsection, we state the GARCH (p,q) model and highlight its main properties. The model is given by the following equation:

Where each

In order to find the optimal vector θ ∈ (ω, α1,…,αq,β1,…,βp) of the parameters defined in equation (1), the most used algorithm of optimization is that from BHHH (Berndt, Hall, Hall and Hausman, Berndt et al.,1974), which maximizes a likelihood function, as in equation (3).8 The iterative optimization method from BHHH for each step is given by:

Where the likelihood function to be maximized, assuming a normal distribution for the error term, satisfies:9

On the other hand, by considering a system of n variables, we can express the error term as:

The error term vector is then modeled as follows:

Here

2.2 Dynamic Conditional Correlation

When studying volatility of diverse variables, the analysis is usually performed with a single equation of the GARCH family.10 However, in order to explore how volatility jointly affects the MFIs’ returns, we use a Dynamic Conditional Correlation (DCC) methodology that allows us to evaluate the impact on their performance (in terms of contagion). This research will now examine the relationship that exists between the conditional correlations and the conditional variances of the returns of the stock prices of the MFIs under study.11

In this work, we focus on the methodology proposed by Engle (2002). Other authors as Bauwens et al. (2003), Wang and Tsay (2013), and Ling and McAleer (2003) propose other extensions of the multivariate-GARCH model with a system of non-related variables. Initially the BEKK model (a Multi-Variable GARCH model) was introduced under a bivariate representation by Engle and Kroner (1995). Under this framework, a generalized multivariate ARCH model can be stated as follows:

Recently, Bauwens et al. (2012) have replaced the BEKK model by other specifications, a DCC model. In this case, it is possible to specify the model (in two steps) in order to obtain a covariance matrix. In this regard, two main dynamic coefficients of correlation were discussed by Engle (2002). On one hand, one of them is the rolling correlation estimator for returns with mean zero, which is defined by:

On the other hand, the coefficient of correlation of exponential smoothing is defined as:

The DCC is defined from the covariance matrix Ht, as follows:12

The matrix Ht can be decomposed, from the following expression:

In this way, it is possible to obtain the dynamic conditional correlation(Rt) from expression (12). The M-variable likelihood maximization can be applied in two steps by GMM optimization (Newey and MacFaden, 1994) according to the optimization methodology proposed by Engle (2002); assuming normally distributed errors as in equations (15) and (16). Hence, the two-step optimization method expressed in aggregated form is:

The first step considers the following objective function:

In the second step, we have

3.Empirical result

3.1 MFIs systems

We present now the results obtained with a system of non-related variables for each MFI (with benchmark variables) for every stock market analyzed. The selection of the GARCH model and the error specification, to obtain the DCCs in each market, are chosen according to the less explosive parameters, see Table 6. The estimations are shown in Table 7. Subsequently, we present the DCCs for each MFIs and their benchmark variables, see Figures 4 and 5. Finally, in Table 7 we calculate the arithmetic and geometric maens for each estimated DCC considering the period of analysis.

Table 6 Model GARCH family (specifications).

| MFIs Systems Not considering ACWI | GARCH Model | Error Specification |

|---|---|---|

| Gentera, IPC, MF | GARCH (1,1) | t-student |

| FI, IPC, ;MF | GARCH (1,1) | t-student |

| BFIL_ NSE, N50, iI50 | GJR-GARCH (1,1) | t-student |

| BFIL_BSE, BD&MFG, BRFL | GJR-GARCH (1,1) | GED |

| BRI, JII, TLK | GARCH (1,1) | Normal |

| Gentera, IPC, ACWI | GARCH (1,1) | Normal |

| FI; IPC, ACWI | EGARCH (1,1) | GED |

| BFIL_NSE, N50, ACWI | GARCH (1,1) | t-student |

| BFIL_BSE, BD&MFG, ACWI | GARCH (1,1) | t-student |

| BRI, JII ACWI | EGARCH (1,1) | t-student |

Note: criteria selection is according to the less explosive parameters.

The results were obtained by using the R software, "fGARCH"library.

Table 7 Econometric results (MFIs and Benchmarks).

| Coef. (1) Std. Err. | Coef. (2) Std. Err. | Coef. (3) Std. Err. | Coef. (4) Std. Err. | Coef. (5) Std. Err. | |||||

|---|---|---|---|---|---|---|---|---|---|

| Gentera_ω | 0.000009 | FI_ω | 0.000083 | BFIL_NSE_ω | 0.000241 | BFIL_BSE_ω | 0.000225 | BRI_ω | 0.000011 |

| (0.000014) | (0.000051) | (0.000121)* | (0.00005)* | (0.000009) | |||||

| Gentera_α | 0.08659 | FI_α | 0.348359 | BFIL_NSE_α | 0.158495 | BFIL_BSE_α | 0.130941 | BRI_α | 0.055043 |

| (0.037231)* | (0.12433)* | (0.049523)* | (0.030491)* | (0.027312)* | |||||

| Gentera_β | 0.89872 | FI_β | 0.650641 | BFIL_NSE_β | 0.618593 | BFIL_BSE_β | 0.629758 | BRI_β | 0.926208 |

| (0.027132)* | (0.136032)* | (0.136525)* | (0.056455)* | (0.016712)* | |||||

| IPC_ω | 0.000001 | IPC_ω | 0.000001 | N50_ω | 0.000003 | BD&MFG_ω | 0.000037 | JII_ω | 0.000006 |

| (0.000002) | (0.000003) | (0.000005) | (0.000004)* | (0.00001) | |||||

| IPC_α | 0.065897 | IPC_α | 0.066201 | N50_α | 0.000003 | BD&MFG_α | 0.02046 | JII_α | 0.09792 |

| (0.02605)* | (0.029512)* | (0.026756) | (0.000026)* | (0.024537)* | |||||

| IPC_β | 0.922272 | IPC_β | 0.921662 | N50_β | 0.928628 | BD&MFG_β | 0.951826 | JII_β | 0.873711 |

| (0.029107)* | (0.032855)* | (0.01574)* | (0.009623)* | (0.053657)* | |||||

| MF_ω | 0.000005 | MF_ω | 0.000005 | iI50_ω | 0.000021 | BRFL_ω | 0.000016 | TLK_ω | 0.000007 |

| (0.000006) | (0.000006) | (0.000009)* | (0.000023) | (0.000003)* | |||||

| MF_α | 0.115317 | MF_α | 0.115912 | iI50_α | 0.036828 | BRFL_α | 0.178185 | TLK_α | 0.044075 |

| (0.028479)* | (0.027632)* | (0.020836)* | (0.091392)** | (0.009175)* | |||||

| MF_β | 0.871226 | MF_β | 0.870042 | iI50_β | 0.822952 | BRFL_β | 0.756588 | TLK_β | 0.937472 |

| (0.039183)* | (0.03935)* | (0.054078)* | (0.165688)* | (0.013027)* | |||||

| DCC_I | 0.022961 | DCC_I | 0.02871 | DCC_I | 0.012854 | DCC_I | 0.018947 | DCC_I | 0.006419 |

| (0.009062)* | (0.009961)* | (0.00433)* | (0.011151)** | (0.005797) | |||||

| DCC_II | 0.928073 | DCC_II | 0.937239 | DCC_II | 0.97705 | DCC_II | 0.914855 | DCC_II | 0.952879 |

| (01.031519)* | (0.02274)* | (0.007167)* | (0.02149)* | (0.028827)v |

Parameters are significant at: 5 % p-value (*) and 10 % p-value (**), respectively.

Source: own elaboration. The results were obtained with the use of the R software, using the libraries: “rugarch” and “rmgarch”.

Source: own elaboration with the use of the R software.

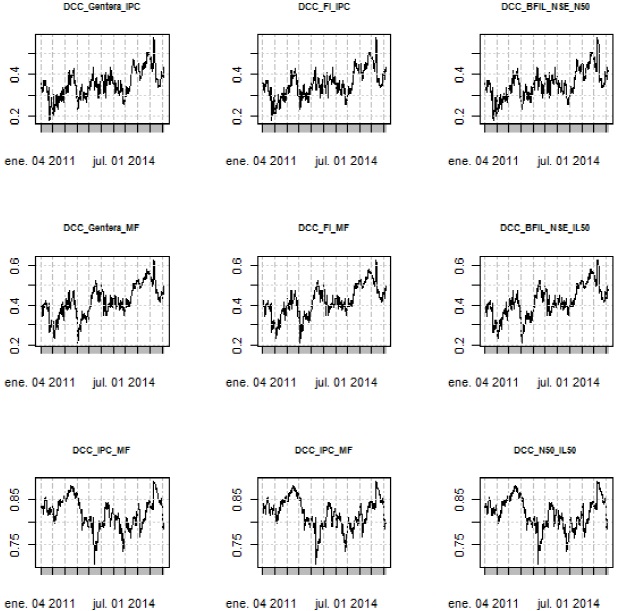

Figure 1 Dynamic Conditional Correlations (MFIs: Gentera, FI, and BFILN SE).

Source: own elaboration with the use of the R software.

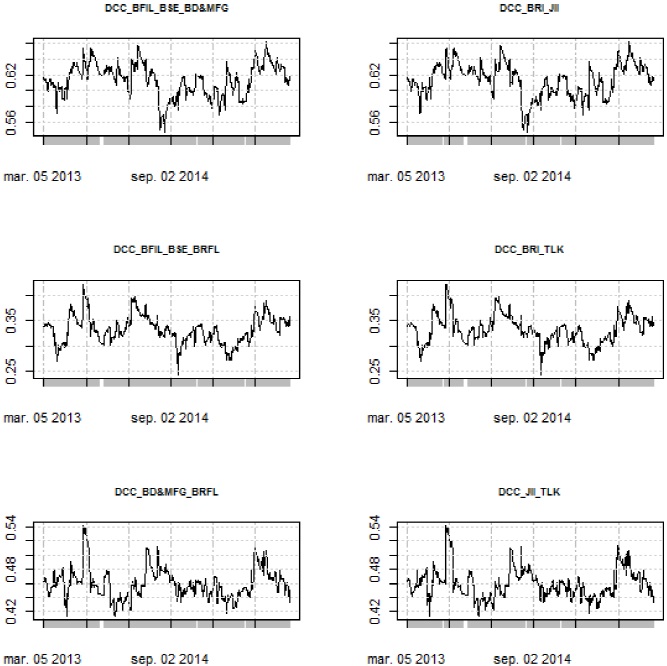

Figure 2 Dynamic Conditional Correlations (MFIs: BF ILBSE, BRI)

Source: own elaboration with the use of the R software.

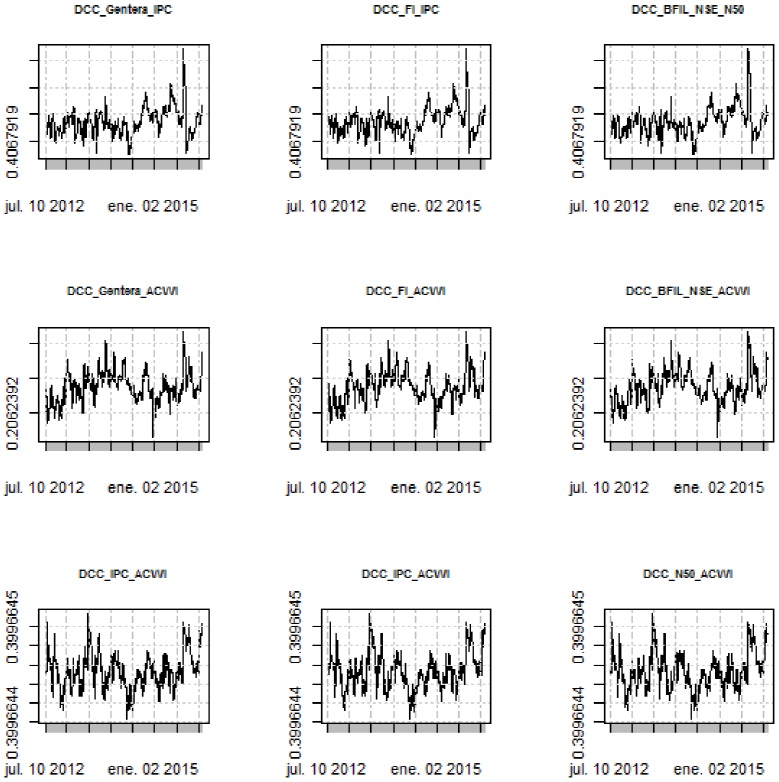

Figure 3 Dynamic Conditional Correlations with ACWI (MFIs: Gentera, FI, and BFILN SE).

Source: own elaboration with the use of the R software.

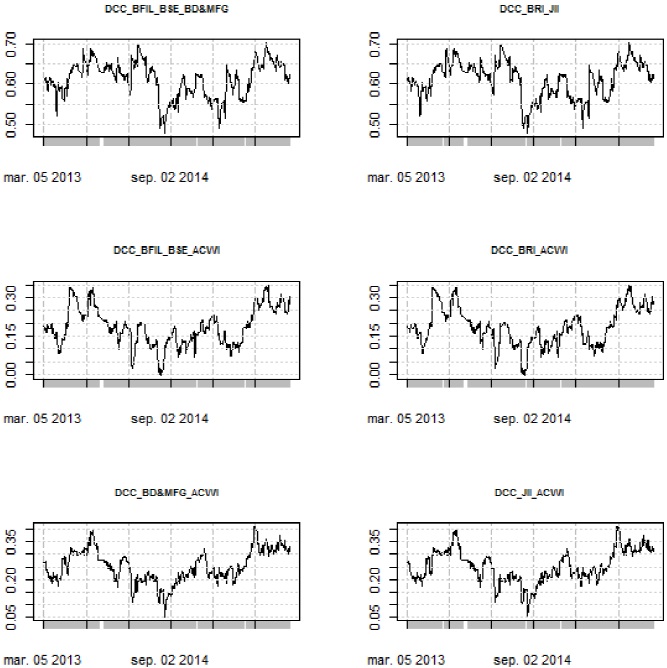

Figure 4 Dynamic Conditional Correlations with ACWI (MFIs: BFILBSE; BRI).

Table 7 shows the estimated coefficients for each MFI and its benchmark variables (based on the criteria in Table 6). The obtained results show that the specification in each equation successfully captures the estimated variances with persistence in both series

It can be also observed in Figures 1 and 2 that it is not possible to appreciate a pattern (or contagion) common in the DCCs in each system of the MFIs. In other words, the particular specifications for each model of the GARCH family, according to the criteria in Table 5, do not capture a common contagion in the volatilities for each MFI. Contagion in volatilities can only be seen in some peaks with high volatility clusters, but not within the entire analysis period. Furthermore, we can see, in Table 8, that the arithmetic and geometric means do not show common patterns in the behavior of the DCCs in the analyzed stock markets.

Table 8 Means of Dynamic Conditional Correlations (DCCs).

| Arithmetic Mean |

Arithmetic Mean |

Arithmetic Mean |

Arithmetic Mean |

Arithmetic Mean |

|||||

|---|---|---|---|---|---|---|---|---|---|

| DCC_Gentera_IPC | 0.43 | DDC_FI_IPC | 0.14 | DCC_BFIL_NSE_N50 | 0.36 | DCC_BFIL_BSE_BD&MFG | 0.28 | DCC_BRI_JII | 0.61 |

| DCC_Gentera_MF | 0.12 | DCC_FI_MF | 0.09 | DCC_BFIL_NSE_iI50 | 0.41 | DCC_BFIL_BSE_BRFL | 0.12 | DCC_BRI_TLK | 0.35 |

| DCC_IPC_MF | 0.22 | DCC_IPC_MF | 0.22 | DCC_N50_iI50 | 0.82 | DCC_BD&MFG_BRFL | 0.13 | DCC_JII_TLK | 0.47 |

| Geometric Mean | Geometric Mean | Geometric Mean | Geometric Mean | Geometric Mean | |||||

| DCC_Gentera_IPC | 0.43 | DCC_FI_IPC | 0.15 | DCC_BFIL_NSE_N50 | 0.35 | DCC_BFIL_BSE_BD&MFG | 0.27 | DCC_BRI_JII | 0.61 |

| DCC_Gentera_MF | 0.11 | DCC_FI_MF | 0.12 | DCC_BFIL_NSE_iL50 | 0.41 | DCC_BFIL_BSE_BRFL | 0.12 | DCC_BRI_TLK | 0.35 |

| DCC_IPC_MF | 0.21 | DCC_IPC_MF | 0.20 | DCC_N50_iI50 | 0.82 | DCC_BD&MFG_BRFL | 0.12 | DCC_JII_TLK | 0.47 |

Source: own elaboration with the use of the R software.

3.2 MFIs systems considering ACWI

In order to analyze the contagion (emphasizing in the analysis of external sources of contagion) in the volatilities of the returns of the MFIs that are listed in the stock market, we use a global reference index, particularly the All Country World Index (ACWI). The latter captures the sources of capital return for 23 emerging markets and 23 developed markets. In the same order of ideas, we can observe, in Table 8, the results obtained with respect to

Table 9 Econometric results including ACWI (MFIs and Benchmarks).

| Coef. -1 Std. Err. |

Coef. -2 Std. Err. |

Coef. -3 Std. Err. |

Coef. -4 Std. Err. |

Coef. -5 Std. Err. |

|||||

|---|---|---|---|---|---|---|---|---|---|

| Gentera_ω | 0.000009 | FI_ω | 0.018425 | BFIL_NSE_ω | 0 | BFL_BSE_ω | 0 | BRI_ω | -0.034736 |

| -0.000016 | -0.01558 | -0.000001 | -0.000001 | (0.000002)* | |||||

| Gentera_α | 0.102476 | FI_α | 0.415963 | BFIL_NSE_α | 0.002846 | BFL_BSE_α | 0.005318 | BRI_α | -0.133189 |

| (0.050604)* | (0.241269)** | (0.000271)* | (0.000493)* | (0.000698)* | |||||

| Gentera_β | 0.883797 | FI_β | 0.959156 | BFIL_NSE_β | 0.996154 | BFL_BSE_β | 0.993681 | BRI_β | 0.995635 |

| (0.024269)* | (0.022523)* | (0.000192)* | (0.000162)* | (0.002131)* | |||||

| IPC_ω | 0.000001 | IPC_ω | -0.234286 | N50_ω | 0.000002 | ED&MFG_ω | 0.000838 | JII_ω | -0.132074 |

| -0.000004 | (0.004241)* | -0.000002v | (0.000138)* | (0.005575)* | |||||

| IPC_α | 0.064805 | IPC_α | -0.128804 | N50_α | 0.047321 | ED&MFG_α | 0.151094 | JII_α | -0.114812 |

| -0.061065 | (0.015623)* | (0.018641)* | (0.073693)* | (0.019883)* | |||||

| IPC_β | 0.921114 | IPC_β | 0.975735 | N50_β | 0.929635 | ED&MFG_β | 0 | JII_β | 0.984505 |

| (0.065666)* | (0.000055)* | (0.022908)* | -0.0152 | (0.000004)* | |||||

| ACWI_ω | 0.000004 | ACWI_ω | -0.509387 | ACWI_ω | 0.000004 | ACWI_ω | 0.000003 | ACWI_ω | -0.406118 |

| (0.000001)* | (0.008383)* | -0.000003 | -0.000009 | (0.008839)* | |||||

| ACWI_α | 0.142967 | ACWI_α | -0.183733 | ACWI_α | 0.131929 | ACWI_α | 0.124324 | ACWI_α | -0.184375 |

| -0.023802 | (0.022734)* | (0.028282)* | (0.054511)* | (0.01155)* | |||||

| ACWI_β | 0.79178 | ACWI_β | 0.94509 | ACWI_β | 0.80366 | ACWI_β | 0.820754 | ACWI_β | 0.959311 |

| (0.032163)* | (0.000083)* | (0.0426)* | (0.088538)* | (0.000129)* | |||||

| DCC_I | 0.030803 | DCC_I | 0.01329 | DCC_I | 0 | DCC_I | 0.019378 | DCC_I | 0.018014 |

| (0.012936)* | (0.004497)* | -0.000071 | (0.011497)* | (0.008203)* | |||||

| DCC_II | 0.884571 | DCC_II | 0.98671 | DCC_II | 0.91982 | DCC_II | 0.891205 | DCC_II | 0.924282 |

| (0.060315)* | (0.00596)* | (0.246352)* | (0.037126)* | (0.087257)* |

Parameters are significant at: 5 % p-value (*) and 10 % p-value (**), respectively.

Source: own elaboration. The results were obtained with the use of the R software, using the libraries: “rugarch” and “rmgarch”.

Finally, we can see in Figures 3 and 4, considering the global index (ACWI) as a point of reference, that it is not possible to observe a common pattern (in terms of contagion) in the DCC for each MFI system. It is worth mentioning that the previous results are similar to those obtained in the preceding section. In this way, the DCC obtained under the specification of the GARCH models do not capture a common contagion in the volatilities of the returns for each MFI. Basically, contagion in volatilities can only be seen in periods of high volatility. Complementing the previous results, it can be observed, in Table 9, that the arithmetic and geometric means do not have common patterns among the DCC of the studied markets.

Table 10 Dynamic Conditional Correlations (DCC).

| Arithmetic Mean |

Arithmetic Mean |

Arithmetic Mean |

Arithmetic Mean |

Arithmetic Mean |

|||||

|---|---|---|---|---|---|---|---|---|---|

| DCC_Gentera_IPC | 0.4 | DCC_FI_IPC | 0.1 | DCC_BFIL_NSE_N50 | 0.42 | DCC_BFIL_BSE_BD&MFG | 0.29 | DCC_BRI_JII | 0.6 |

| DCC_Gentera_ACWI | 0.28 | DCC_FI_ACWI | 0.14 | DCC_BFIIL_NSE_ACWI | 0.21 | DCC_BFIL_BSE_ACWI | 0.19 | DCC_BRI_ACWI | 0.19 |

| DCC_IPC_ACWI | 0.62 | DCC_IPC_ACWI | 0.58 | DCC_N50_ACWI | 0.41 | DCC_BD&MFG_ACWI | 0.13 | DCC_JII_ACWI | 0.25 |

| Geometric Mean | Geometric Mean | Geometric Mean | Geometric Mean | Geometric Mean | |||||

| DCC_Gentera_IPC | 0.39 | DCC_FI_IPC | 0.13 | DCC_BFIL_NSE_N50 | 0.42 | DCC_BFIL_BSE_BD&MFG | 0.29 | DCC_BRI_JII | 0.6 |

| DCC_Gentera_ACWI | 0.27 | DCC_FI_ACWI | 0.14 | DCC_BFIL_NSE_ACWI | 0.21 | DCC_BFIL_BSE_ACWI | 0.19 | DCC_BRI_ACWI | 0.18 |

| DCC_IPC_ACWI | 0.62 | DCC_IPC_ACWI | 0.58 | DCC_N50_ACWI | 0.41 | DCC_BD&MFG_ACWI | 0.13 | DCC_JII_ACWI | 0.24 |

Source: own elaboration with the use of the R software.

4. Conclusions

This research has shown that there is not a pattern between long-term memory and liquidity in the studied MFIs. According to the analysis carried out on the DCC-M-GARCH approach, the effects of contagion (in MFIs returns) only occur in periods of high volatility when considering local benchmark variables. Moreover, when considering the global index All Countries World Index (ACWI), the results confirm the empirical evidence.

As a recommendation arising from the empirical findings, the MFIs that obtain resources via the stock market should operate with efficient methodologies in the selection of clients, which will impact in their level of liquidity in the stock market. It is also recommended for investors, both institutional and individual, consider MFIs in their investment portfolios in stability periods given that contagion only occurs in periods of high volatility.