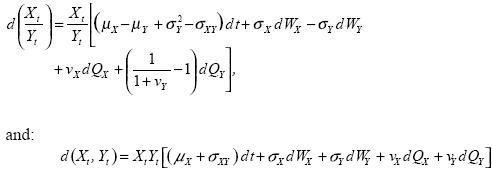

APPENDIX: ITÔ'S LEMMA ON THE RATIO OF TWO PROCESSES

In this appendix we state without proof 5 a couple of useful results, in the development of this paper, for mixed diffiision–jump processes. Given the homogeneous linear stochastic differential equations:

where dQX are dQY uncorrelated Poisson processes and dWX, dWY are Wiener processes satisfying Cov(dWX, dWY) = ρXY dt, and the Poisson processes are independent of trie Wiener processes, then the stochastic differentials of the ratio Xt/Yt and of the product Xt Yt , are given, respectively, by:

5 For the proofs, we refer the reader to Gihman and Skorohod (1972).