nueva página del texto (beta)

nueva página del texto (beta) Inglés (pdf)

Inglés (pdf)

Artículo en XML

Artículo en XML Referencias del artículo

Referencias del artículo

Enviar artículo por email

Enviar artículo por email Citado por SciELO

Citado por SciELO  Similares en

SciELO

Similares en

SciELO

Permalink

PermalinkIntroduction

The implementation of the Accrual-Based Government Accounting Standards in the ministries/institutions that began in 2015 by using the Accrual-Based Accounting System of Institutions Application. The stipulation of the regulation on the accrual-based Government Accounting Standards signed by the President required all government agencies, both at the central and regional levels, to implement the Accrual-Based Government Accounting Standards started from January 1, 2015. The legal basis of the accrual-based Government Accounting Standards is the Government Regulation Number 71 of 2010 on Government Accounting Standards. Accrual-Based Accounting System of Institutions Application is the development of the Accounting System of Proxy of Budget User which was used prior to 2015 by using the cash-based financial statements. The Accrual-Based Accounting System of Institutions application is still under development, so it often requires updates to update the existing features of the application. Given the change in the government accounting base from cash to accruals to a full accrual basis, the local financial management apparatus is required to develop an understanding in accounting. To get the competent apparatus in this field, this is not apart from the educational background, training and work experience that is owned by the financial management apparatus itself. Financial management apparatus that controls government accounting is needed in preparation and preparation of financial statements that must be prepared in an orderly manner following applicable government accounting standards. The financial statements are principally the regional government management assertions that contain and present complete financial information as a basis for the government to make economic and financial decisions and to fulfill the government’s accountability aspects in managing regional finances according to the regulatory mandate entrusted to them (Eriadi et al., 2018; Muda and Naibaho, 2018 & Muda and Hutapea, 2018). Regional government financial statements essentially contain all financial performance achievements during the accounting period regarding revenue and expenditure achievements, achievement of assets and liabilities growth and equity as well as a real picture of expenses and financing.

The information system user satisfaction can be used as a measurement for the success of an information system. User satisfaction then becomes a part in the development model of the success of information system. The information system that meet the needs and expectations of the users is the high-quality information system, which is fast in displaying information, actual, can be used as a consideration in decision making and suitable to the desired needs. In order to meet the needs of a good information system, it requires a good design system, as well as a good programming system and is able to ease the user by providing and developing various facilities to access the information. The key to success in satisfying users of information system is in the quality of services provided by the information system providers. The benefits of information technology in building an individual, company, and even a country are very big impact. Proven that IT can change an Individual, a company, even an organization and country (Winter et al, 2009). The Information system success model that is widely used is the DeLone and McLean (2003) model which states that information quality, system quality and service quality will have a positive effect on user satisfactionWoodham et al., 2017; Hussain et al., 2017; Filieri et al., 2017; Lin, 2017; Efthymiou and Antoniou, 2017; Kim et al., 2017; Radu et al., 2017; Hong et al. 2017 Berger et al., 2017; Carrasco et al., 2017; Yousuf and Wahab, 2017; Laumer et al., 2017; Kiran and Diljit, 2017; Balaji et al., 2017; Yang, 2017; Noutsa et al., 2017; Ryu and Lee., 2017; Cleverley et al., 2017 and Kilsdonk et al., 2017. A study conducted by Iivari (2005) that empirically tested the DeLone and McLean model, proved that the success of information system is influenced by the quality of information system and the quality of information generated from the related system. Human resources as the application users have a direct connection with the implementation of the system. Therefore, the competence of application users is a very important factor in the successful implementation of information system. The challenges faced by human resource competencies are competency methods to meet significant future challenges. In order to utilize strategies based on efficient human resource development, the needs of organizational leaders and the needs of human resource practitioners to make a number of basic decisions may face several challenges. The role of human resource management has shifted from traditional management that only manages people in organizations, to strategic human resource management to make decisions according to environmental changes that are very fast and difficult to predict. The ability of managers or managers to balance organizational changes with internal factors and external factors is the key to the success of a business activity.

The purpose of this study is to support of the Adaptive Behavior Assessment System (ABAS) Theory where quality and information quality systems impact on the User satisfaction. Almost every organization activity is currently using technology. Information technology revolution occurs in organizational activities, from manual systems to computerized systems. Simple information systems can be said to be processing data and then transforming it into information. In simple terms it can be said that a system of information and processing data, and then turn it into information. The Information System involves all organizational components related to input (data) activities, output (information), and also users. Information flow in the organization flows vertically and horizontally. The information systems and human resources involved are very important components in the success of the organization both engaged in business and non-business. The most challenging task facing the organization is the effectiveness of implementing information technology. This role requires human resources who can absorb, understand and adapt with new things. Within the scope of the information technology requires the user to be adaptive to change and progress. Information systems will never develop by themselves, but need to be supported by many factors that can be effective. The success of the development of information systems depends very much on the suitability of expectations between systems analysts, users, sponsors and customers. The development of information systems requires careful planning and implementation, to avoid rejection of the system being developed. If the information system is used optimally, it can improve the quality of information and increase user satisfaction.

Literature review

Adaptive Behavior Assessment System (ABAS) Theory

Adaptive behavior is the level of ability/effectiveness of a person in meeting the standards of personal independence and social responsibility expected for age and group culture (American Association on Mental Deficiency/AAMD, 1983). Adaptive behavior is a person’s self and social maturity in carrying out everyday activities in accordance with age and related to the culture of the group and adaptive behavior is self and social maturity (Gresham and Elliot, 1987; Rust et al, 2004; Krichmar, 2008; Oakland and Harrison, 2011; Price et al., 2018 and James et al., 2018). Someone in carrying out general daily activities in accordance with age conditions and related to group culture. The concept of adaptive behavior:

Adaptive behavior focuses on everyday behavior.

Fulfillment of the expectations of the community & environment where the person concerned lives.

The ability to effectively cope with the conditions that are happening in the community.

The concept of social ability/adaptive behavior can be interpreted as a person’s ability to master social speech in their environment. The ability to adapt to the demands of the environment or the application of new systems that are displayed in the form of capabilities:

Independent functioning/function of independence: ability to achieve success in carrying out tasks according to age and hope.

Personal responsibility: ability monitor his personal behavior and can accept all risks from a sense of responsibility for making a decision.

Social responsibility: social adjustment to the environment, emotional development, acceptance of feelings and responsibilities around it.

In the adaptive structure the technological characteristics of the technology are reflected in features and general spirit. The use of organizational resources in the form of regulations, values, agreements so as to bring about an appropriate use attitude towards the technology of consensus level between users. The assumptions, expectations, and knowledge of people about information technology affect the acceptance of information technology applications in an organization (Orlikowski and Gash, 1991; Karanasios, 2018). The gap in understanding between system users and system analysts arises due to gaps in cognitive frames. Every information processing is mediated by categorizers and imposition of concepts. These categories and concepts are actually is a model/imitation) about the world around. This model contains knowledge structures or cognition structures.

The Information System Success Model

Examining the success of an information system is an important thing for an organization which is implementing a new information system. DeLone & McLean (1992) and Gao and Park (2017) proposed a model to measure the success of information system in organizational level. DeLone and McLean proposed a theory about the success of information system known as the Delone and McLeon success model which consists of:

System quality is used for measuring the quality of system of the information technology itself.

Information quality is used for measuring the output quality of the information system.

Use is the use of the output of a system by the receiver/user.

User satisfaction is the response provided by the user in response to the use of the output of information system.

Individual impact is the effect of information on user behavior.

Organizational impact is the effect of information on organizational performance.

Factors of success of information systems in an organization because of the quality characteristics of the system itself that can be replicated, the quality of the information system output, consumption of output, user response to the information system, the influence of information systems on user habits and their influence on organizational performance. system quality and information quality, individually and together, affect the satisfaction of its users. A quality information system that can meet the needs will satisfy its users and optimize the performance of users and their organizations so that the organization will support the information system technology.

Human Resources (HR) Quality

Human resources (HR) are the people who are in an organization who contribute through their thoughts and perform various jobs in achieving the organizational goals. The contribution is the thought that they have in various activities within the organization (Muda and Dharsuky, 2015, Mendoza et al., 2011; Cheuk et al., 2017; Iannacci and Comford, 2017; Achamad et al., 2017; Zerbino et al. 2017; Tam et al., 2017; Hernandez-Ortega et al., 2017; Sánchez et al., 2017; Almazán et al., 2017; Alzahrani, et al., 2017; Shin et al., 2017; Horvath and Bauermeister, 2017; Hsu et al., 2017; Muda et al., 2018; Muda and Erlina, 2018 & Pohan et al., 2018). The ability of the organization to deliver its goals is determined by the quality of human resources owned by the organization. Therefore, Human Resources is one of the important elements in the organization (Dalimunthe et al., 2016; 2017 and Gusnardi et al., 2016). Human resource development can basically be done in various ways, but in principle, it is to increase human resource competence. Development improvements can be done through education, training, motivation and various key human resource programs Human Resources is the main pillar which supports and drives the organization in the effort to realize the vision and mission of the organization. The key to success above depends on the human resource infrastructure as follows: 1. how is the readiness of human resources to achieve the desired results. 2. how the right human with the right skills at the right place and the right cost. 3. Human resource needs. As well as the ability to adapt to changes to maintain humans who are ready for the next arrival

Research method

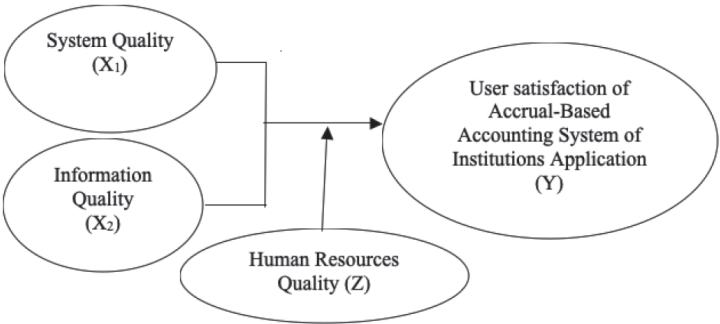

This type of research is explanatory research. An explanatory study which is a study that explains the causal relationship between research variables with hypothesis testing. In explanatory research, the approach used in this research is survey method that is research done to obtain facts about phenomena that exist in research object and searching actual and systematic information (Lutfi et al., 2016; Yahya et al., 2017; Syahyunan et al., 2017; Tarmizi et al., 2017; Badaruddin et al., 2017; Muda and Nurlina, 2018 and Muda et al., 2018). This research applied survey method with census sampling technique. The population in this research is the operators of Accrual-Based Accounting System of Institutions Application in the service partner work units of Indonesia with the total of 209 work units, where each work unit will be given 1 (one) questionnaire to be filled by the operators. The instrument of this research was a questionnaire designed by the researcher based on the adaptation on the research conducted by Libby (2017); Alalwan et al., (2017); Visinescu et al., (2017); Nasution (2016); Lubis et al., (2016) and Muda et al., (2017). The variables of this research were measured by using the scale of interval measurement, through the questionnaire with a score ranging from 1 to 5. The operational definitions and measurement scale are briefly described in the following Table:

Table 1 Operational Definitions

| Variable | Definition of Variable | Variable Measurement | Scale |

| Dependent Variable | |||

| User satisfaction of Accrual-Based Accounting System of Institutions application (Y) | The response of the users of application (operators) on Accrual-Based Accounting System of Institutions application and the output resulted from Accrual-Based Accounting System of Institutions application. |

|

Interval |

| Independent Variable | |||

| System Quality (X1) | The Quality of the used Accrual-Based Accounting System of Institutions application, perceived from the perception of the users of the application (operators). |

|

Interval |

| Information Quality (X2) | The Quality of information (output) resulted from the used Accrual-Based Accounting System of Institutions application, perceived from the perception of the users of the application (operators). |

|

Interval |

| Moderating Variable | |||

| Human Resources Quality (Z) | The ability of the operators in performing their tasks in financial management. |

|

Interval |

The data analysis used in this research was Partial Least Square (PLS)approach. PLS is a component- or variance-based equation model of Structural Equation Modelling (SEM). PLS is an alternative approach that shifts from the Covarian-based to variance-based SEM approach (Ghozali and Latan, 2015). This SEM test used SmartPLS version 3.0 program.

Results and discussion

Measurement Model (Outer Model)

The measurement model was used to test the validity of the construct and the reliability of the instrument (Abdillah and Jogiyanto, 2015; Tarmizi et al., 2016 & Sihombing et al., 2017). The validity test of the construct used two methods, they were convergent validity and discriminant validity, while the reliability test of the construct used composite reliability (Sirojuzilam et al, 2016 & 2017).

Convergent Validity

An indicator is said to be valid if it has a loadings factor of more than 0,5 and an average variance extracted (AVE) value of more than 0,50 towards the target construct (Muda and Hasibuan, 2018). The AVE values from the result of PLS Algorithm of SmartPLS program can be seen in the following Table 2:

Table 2 Average Variance Extracted (AVE) Values

| Variable | Average Variance Extracted (AVE) | Information |

| System Quality (X1) | 0.669 | Valid |

| Information Quality (X2) | 0.653 | Valid |

| Human Resources Quality (Z) | 0.795 | Valid |

| User Satisfaction (Y) | 0.607 | Valid |

| Human Resources Quality*System Quality | 0.585 | Valid |

| Human Resources Quality*Information Quality | 0.626 | Valid |

Source: Data processed (2017).

The loadings factor and AVE values resulted from PLS Algorithm of SmartPLS program can be seen in the following Table 3:

Table 3 Loadings Factor Values

| Variable | Indicator | Loadings Factor | Information | Indicator | Loadings Factor | Information |

| System Quality (X1) | KS1 | 0.819 | Valid | KS4 | 0.810 | Valid |

| KS2 | 0.893 | Valid | KS5 | 0.842 | Valid | |

| KS3 | 0.772 | Valid | KS6 | 0.766 | Valid | |

| Information Quality (X2) | KI1 | 0.813 | Valid | KI4 | 0.811 | Valid |

| KI2 | 0.856 | Valid | KI5 | 0.789 | Valid | |

| KI3 | 0.757 | Valid | KI6 | 0.818 | Valid | |

| Human Resources Quality (Z) | SDM1 | 0.912 | Valid | SDM4 | 0.937 | Valid |

| SDM2 | 0.907 | Valid | SDM5 | 0.815 | Valid | |

| SDM3 | 0.883 | Valid | ||||

| User Satisfaction (Y) | KP1 | 0.828 | Valid | KP6 | 0.617 | Valid |

| KP2 | 0.828 | Valid | KP7 | 0.711 | Valid | |

| KP3 | 0.872 | Valid | KP8 | 0.604 | Valid | |

| KP4 | 0.838 | Valid | KP9 | 0.806 | Valid | |

| KP5 | 0.850 | Valid | KP10 | 0.782 | Valid | |

| Human Resources Quality*System Quality | SDM1 * KS1 | 0.564 | Valid | SDM3 * KS4 | 0.550 | Valid |

| SDM1 * KS2 | 0.654 | Valid | SDM3 * KS5 | 0.600 | Valid | |

| SDM1 * KS3 | 0.532 | Valid | SDM3 * KS6 | 0.598 | Valid | |

| SDM1 * KS4 | 0.533 | Valid | SDM4 * KS1 | 0.584 | Valid | |

| SDM1 * KS5 | 0.543 | Valid | SDM4 * KS2 | 0.679 | Valid | |

| SDM1 * KS6 | 0.588 | Valid | SDM4 * KS3 | 0.573 | Valid | |

| SDM2 * KS1 | 0.558 | Valid | SDM4 * KS4 | 0.547 | Valid | |

| SDM2 * KS2 | 0.652 | Valid | SDM4 * KS5 | 0.580 | Valid | |

| SDM2 * KS3 | 0.568 | Valid | SDM4 * KS6 | 0.611 | Valid | |

| SDM2 * KS4 | 0.528 | Valid | SDM5 * KS1 | 0.524 | Valid | |

| SDM2 * KS5 | 0.547 | Valid | SDM5 * KS2 | 0.587 | Valid | |

| SDM2 * KS6 | 0.573 | Valid | SDM5 * KS3 | 0.511 | Valid | |

| SDM3 * KS1 | 0.551 | Valid | SDM5 * KS4 | 0.522 | Valid | |

| SDM3 * KS2 | 0.632 | Valid | SDM5 * KS5 | 0.554 | Valid | |

| SDM3 * KS3 | 0.553 | Valid | SDM5 * KS6 | 0.551 | Valid | |

| Human Resources Quality*Information Quality | SDM1 * KI1 | 0.615 | Valid | SDM3 * KI4 | 0.565 | Valid |

| SDM1 * KI2 | 0.647 | Valid | SDM3 * KI5 | 0.615 | Valid | |

| SDM1 * KI3 | 0.582 | Valid | SDM3 * KI6 | 0.608 | Valid | |

| SDM1 * KI4 | 0.608 | Valid | SDM4 * KI1 | 0.633 | Valid | |

| SDM1 * KI5 | 0.678 | Valid | SDM4 * KI2 | 0.657 | Valid | |

| SDM1 * KI6 | 0.630 | Valid | SDM4 * KI3 | 0.577 | Valid | |

| SDM2 * KI1 | 0.650 | Valid | SDM4 * KI4 | 0.616 | Valid | |

| SDM2 * KI2 | 0.668 | Valid | SDM4 * KI5 | 0.665 | Valid | |

| SDM2 * KI3 | 0.656 | Valid | SDM4 * KI6 | 0.645 | Valid | |

| SDM2 * KI4 | 0.615 | Valid | SDM5 * KI1 | 0.596 | Valid | |

| SDM2 * KI5 | 0.679 | Valid | SDM5 * KI2 | 0.540 | Valid | |

| SDM2 * KI6 | 0.636 | Valid | SDM5 * KI3 | 0.547 | Valid | |

| SDM3 * KI1 | 0.630 | Valid | SDM5 * KI4 | 0.521 | Valid | |

| SDM3 * KI2 | 0.639 | Valid | SDM5 * KI5 | 0.523 | Valid | |

| SDM3 * KI3 | 0.544 | Valid | SDM5 * KI6 | 0.594 | Valid | |

| Human Resources Quality*Service Quality | SDM1 * KL1 | 0.632 | Valid | SDM3 * KL3 | 0.573 | Valid |

| SDM1 * KL2 | 0.625 | Valid | SDM3 * KL4 | 0.540 | Valid | |

| SDM1 * KL3 | 0.642 | Valid | SDM4 * KL1 | 0.640 | Valid | |

| SDM1 * KL4 | 0.596 | Valid | SDM4 * KL2 | 0.624 | Valid | |

| SDM2 * KL1 | 0.619 | Valid | SDM4 * KL3 | 0.643 | Valid | |

| SDM2 * KL2 | 0.586 | Valid | SDM4 * KL4 | 0.597 | Valid | |

| SDM2 * KL3 | 0.630 | Valid | SDM5 * KL1 | 0.534 | Valid | |

| SDM2 * KL4 | 0.576 | Valid | SDM5 * KL2 | 0.508 | Valid | |

| SDM3 * KL1 | 0.572 | Valid | SDM5 * KL3 | 0.519 | Valid | |

| SDM3 * KL2 | 0.564 | Valid | SDM5 * KL4 | 0.531 | Valid |

Source: Data processed (2017).

Discriminant Validity

If the square root value of AVE of each construct is greater than the correlation value between a construct and another construct in the model, it can be said that it has a good discriminant validity value (Fornnel and Larcker, 1981 in Ghozali and Latan, 2015). The square root values of AVE resulted from the PLS Algorithm of SmartPLS program can be seen in the following Table 4:

Table 4 Square Root Values of AVE

| Variable | Information Quality (X2) | User Satisfaction (Y) | System Quality (X1) | Human Resources Quality (Z) | Human Resources Quality * System Quality | Human Resources Quality * Information Quality |

| Information Quality (X2) | 0.808 | |||||

| User Satisfaction (Y) | 0.497 | 0.779 | ||||

| System Quality (X1) | 0.369 | 0.537 | 0.818 | |||

| Human Resources Quality (Z) | 0.223 | 0.441 | 0.218 | 0.892 | ||

| Human Resources Quality * System Quality | 0.016 | 0.391 | 0.100 | -0.036 | 0.765 | |

| Human Resources Quality * Information Quality | -0.179 | 0.330 | 0.005 | 0.050 | 0.480 | 0.791 |

Source: Data processed (2017).

Composite Reliability

Ghozali and Latan (2015) stated that a latent variable has a high reliability if it has a composite reliability value of more than 0.60. The composite reliability values resulted from the PLS Algorithm of SmartPLS program can be seen in the following Table 5:

Table 5 Composite Reliability Values

| Variable | Composite Reliability | Information |

| System Quality (X1) | 0.924 | Reliable |

| Information Quality (X2) | 0.918 | Reliable |

| Human Resources Quality (Z) | 0.951 | Reliable |

| User Satisfaction (Y) | 0.938 | Reliable |

| Human Resources Quality * System Quality | 0.977 | Reliable |

| Human Resources Quality * Information Quality | 0.980 | Reliable |

Source: Data processed (2017).

R-square

The higher the R² value, the better the prediction model of the proposed research model. A strong model is shown by the value of 0.67, a moderate model is shown by the value of 0.33 and a weak model is shown by the value of 0.19 (Chin, 1998 in Ghozali and Latan, 2015; Handoko et al., 2017; Situmorang et al., 2017; Sadalia et al., 2017 and Erlina and Muda, 2018). The R² value is used to explain the effect of the latent (independent) variable on the latent (dependent) variable or how great the effect is. The R-square value resulted from PLS Algorithm of SmartPLS program can be seen in the following Table 6:

Hypothesis test

The hypothesis test used the significance level of 5% and confidence level of 95%. In order to make a hypothesis accepted (Syahyunan, et al., 2017; Nurlina et al., 2017; Ferine et al., 2017; Sari et al., 2018; Sadalia et al., 2018; Erlina and Muda, 2018 and Erwin et al., 2018) it has to have a t-statistics value > 1,96. Table 7 shows the results of path coefficients and t-statistics.

Table 7 The Path Coefficients and t Statistics Values

| Original Sample (O) | Sample Mean (M) | Standard Deviation (STDEV) | T Statistics (|O/STDEV|) | p Values | Information | |

| KI -> KP | 0.360 | 0.363 | 0.090 | 3.983 | 0.000 | Hypothesis is accepted (p<0.05) |

| KS -> KP | 0.316 | 0.314 | 0.073 | 4.362 | 0.000 | Hypothesis is accepted (p<0.05) |

| KSDM -> KP | 0.287 | 0.291 | 0.084 | 3.431 | 0.001 | Hypothesis is accepted (p<0.05) |

| Moderating Effect 1 -> KP | 0.316 | 0.303 | 0.127 | 2.496 | 0.013 | Hypothesis is accepted (p<0.05) |

| Moderating Effect 2 -> KP | 0.342 | 0.371 | 0.143 | 2.395 | 0.017 | Hypothesis is accepted (p<0.05) |

Source: Data processed (2017).

Discussion

Based on the results of the test in Table 7, the effect of each variable is described as follows:

The effect of system quality on user satisfaction

The system quality variable (X1) has a t-statistics value of 4,362 which is greater than 1,96 and a positive path coefficient value, thus, hypothesis 1 is accepted. It can be concluded that the system quality variable has a significant positive effect on the user satisfaction of Accrual-Based Accounting System of Institutions application. The results of this study support the success model of information system proposed by DeLone & McLean (2003), Seddon and Kiew (1996), Iivari (2005), Petter,et al., (2013); Abdillah and Jogiyanto, (2015); Lubis et al., (2016); Libby (2017); Alalwan et al., (2017); Visinescu et al., (2017); Hariguana et al., (2017); Wang and Lin, (2017); Vischer and Wifi et al., (2017); McKnight et al., (2017); Li et al., (2017); Hamari, et al., (2017); Chen et al., (2017); Ren et al., (2017); Luo and Chea, (2017); Uppal et al., (2017) and Shang et al., (2017). Security is very important to prevent the misuse or changes of the data for personal purposes. In order to be able to access this application, the username and password are used for security purposes. It is more on the fulfillment of the needs of the institutions since this application adopts the business processes of the activities of the institutions, so that the features of this application are suited to the needs of the users.

The effect of information quality on user satisfaction

The information quality variable (X2) has a T-statistics value of 3.983 which is greater than 1.96 and a positive path coefficient value, thus, hypothesis 2 is accepted. It can be concluded that the information quality variable has a significant positive effect on user satisfaction of Accrual-Based Accounting System of Institutions application. The results of this study support the success model of information system proposed by DeLone & McLean (2003), Seddon and Kiew (1996), Livari (2005), Rostaminezhad et al, 2013; Muda et al., 2016; Libby (2017); Alalwan et al., (2017); Visinescu et al., (2017); Muda et al., (2017), Diavastisa et al., (2017); Gorla et al., (2017); Dooley et al., (2017); Tarí et al., 2017; Barata and Cunha, 2017; Liu et al., 2017; Liang et al., 2017; Sun and Teng, (2017); Gao et al., (2017); Hsieh and Lin, (2017) and Hsu et al., (2017). The Accrual-Based Accounting System of Institutions application makes the recording and reporting processes which previously took a longer time to be faster and easier. It makes the information resulted from the application is useful for consideration in making decisions as it is available when needed.

The effect of human resources quality on user satisfaction

The human resources quality variable (X4) has a T-statistics value of 3.431 which is greater than 1.96 and a positive path coefficient, thus, hypothesis 4 is accepted. It can be concluded that the human resources quality variable has a positive significant effect on the user satisfaction of Accrual-Based Accounting System of Institutions application. The results of this study are in line with the results of the research conducted by Mendoza et al., 2011; Cheuk et al., 2017; Iannacci and Comford, 2017; Zerbino et al. 2017; Tam et al., 2017; Hernandez-Ortega et al., 2017; Sánchez et al., 2017; Almazán et al., 2017; Alzahrani, et al., 2017; Shin et al., 2017; Horvath and Bauermeister, 2017 and Hsu et al., 2017. The operator of work unit is the most associated party with the operations of Accrual-Based Accounting System of Institutions application. Human resources as the users of application have a direct connection with the implementation of the system. Therefore, the competence of the users of application is a very important factor in the successful implementation of Accounting Information System (SIA).

Human resources quality moderates the relationship between system quality and user satisfaction

The Human Resources quality variable system quality has a T-statistics value of 2.496 which is greater than 1.96 and a positive path coefficient value, thus, hypothesis 5 is accepted. It can be concluded that human resources quality can mderate the relationship between the system quality and user satisfaction of Accrual-Based Accounting System of Institutions application. The research conducted by Mendoza et al., 2011; Cheuk et al., 2017; Iannacci and Comford, 2017; Zerbino et al. 2017; Tam et al., 2017; Hernandez-Ortega et al., 2017; Sánchez et al., 2017; Almazán et al., 2017; Alzahrani, et al., 2017; Shin et al., 2017; Horvath and Bauermeister, 2017 and Hsu et al., 2017 stated that the participation of information system users is expected to improve the quality of information system, because an information system will not be effective in assisting the work if it does not involve the users of accounting information system. The users of accounting information system who obtain ability from a training program or education and experience can increase their satisfaction in the use of the applied accounting information system.

Human resources quality moderates the relationship between information quality and user satisfaction

The human resources quality information quality has a T-statistics value of 2.395 which is greater than 1.96 and a positive path coefficient, thus, hypothesis 6 is accepted. It can be concluded that human resources quality can moderate the relationship between the information quality and user satisfaction of Accrual-Based Accounting System of Institutions application. The qualified human resources will be able to carry out the accounting information system by understanding and applying the logic of accounting well according to the prevailing regulations. The human resources of the Government who fail to understand and apply the logic of accounting will have an impact on the mistakes in making financial statements and mismatch reports with the standards set by the government (Jung, 2017; Sforza and Cimini, 2017; Muda et al., 2017, Agasisti et al.,2017; Fuchs et al., 2017; Cohen et al., 2017 and Caperchione et al., 2017). The Accrual-Based Accounting System of Institutions application is a financial system that is stored online with the goal of transparency for each party. This system is applied as an accrual based budgeting documentation. Everyone can access the budget data compiled by a local government so that it is expected to prevent the embezzlement of funds or fraud from the local bureaucracy (Yahya et al., 2017). Monitoring financial data as well as its control by the public is a practice of financial democratization in a local government. Citizens can immediately issue a complaint if they suspect undue data. They can also ascertain whether the paid tax funds are being used properly. Public transparency is an obligation of every local government to prevent and anticipate all fraudulent acts in the management of state finances. The thing that is considered in the organization is the morale of each employee. The spirit of employees is important because it can increase productivity. Employees who have low morale tend to generate financial costs in the organization, while employees who have a high morale tend to generate financial benefits within the organization.

Conclusions

The conclusions of this study are as follows:

System quality has a significant positive effect on the user satisfaction of Accrual-Based Accounting System of Institutions application in the service partner work units of Indonesia Government. The higher the value of system quality the higher the level of user satisfaction of the Accrual-Based Accounting System of Institutions application. The level of satisfaction includes content satisfaction, accuracy, appearance, ease of use and pertinence. These results support the Adaptive Behavior Assessment System (ABAS) Theory in which behavioral analysis experiments find a large number of principles of statements about how content satisfaction, accuracy, appearance, ease of use and pertinence as a function of environmental variables. The tactics for changing behavior are derived from principles that have also been applied, in a more effective and sophisticated way, for most human behavior in a variety of natural settings. Humans are created to be able to learn with a range of extraordinary behavior. The series of responses, sometimes seemingly not included in the organization of logic, supports the complexity of human behavior. The System quality and information quality together affect to the user satisfaction. The amount of use can affect user satisfaction positively. The user satisfaction affect on individual impact and then affect to the organizational impact. Information systems have a role in supporting operational business activities, supporting management in decision making, and supporting the advantages of an organization’s competitive strategy. Information systems can be used to create strategic advantages. Strategic excellence is an advantage that has a fundamental impact in shaping the organization’s operations.

Information quality has a significant positive effect on the user satisfaction of Accrual-Based Accounting System of Institutions application in the service partner work units of Indonesia Government. The higher the acceptance levels the more accurate, trustable, on time, relevant, understandable and detailed. These results support the Adaptive Behavior Assessment System (ABAS) Theory in which Information quality generated from the Information system in the modern business competition climate plays a very important role so as to be able to create, manipulate and capture information problems that develop both internally and externally. The effectiveness of information systems will be useful for management of a business entity to make changes to business development strategies. The use of an information system is expected to provide competitive advantage and comparative advantage for the company. Implementation of effective and efficient information technology is expected to be a success factor for a business entity.

Human Resources quality has a significant positive effect on the user satisfaction of Accrual-Based Accounting System of Institutions application in the service partner work units of Indonesia Government. The better the educational background, experience, the amount of training and know the ins and outs of accounting and professional in their field, the better the application of Accrual-Based Accounting System. Changes from manual systems to computerized systems not only involve changes in technology but also changes in behavior and organization. Therefore, the main impact of information technology is mediated by a number of factors, many of which require an in-depth understanding of the organizational context and human behavior. These results support the Adaptive Behavior Assessment System (ABAS) Theory where Human Resources quality supports the development of Information Technology. Human Resources quality has an effect on the user satisfaction of Accrual-Based Accounting System of Institutions application on the ease and smoothness of information or data processing. Human Resources quality supports the information technology function as retrieving, collecting, processing, storing, distributing, and presenting information will facilitate the Personnel Management process to manage its human resources well and quickly, of course by minimizing possible human errors. This is what makes these two aspects mutually connected and synchronized.

Human Resources quality can moderate the relationship between the system quality and user satisfaction of Accrual-Based Accounting System of Institutions application in the service partner work units of Indonesia Government. The Human Resources function serves as the moderating variable of the relationship between System Quality and the Flexibility, Security, Correctable, Understandable and Ease of Use indicators of the user satisfaction of the Accrual-Based Accounting System of Institutions application. These results support the Adaptive Behavior Assessment System (ABAS) Theory where Human Resources quality supports moderated the relationship between the system quality and user satisfaction of Accrual-Based Accounting System of Institutions application. Organizations are required to be more responsive to users and can improve the quality of users. Service quality and user satisfaction are important because the user’s trust in the quality of the system is a construct that determines the possibility of a repeat purchase from the user and ultimately affects the success of an organization. User satisfaction is one of the factors to measure success for every development and implementation of information application systems in an organization. A good quality service image is not based on the perspective or perception of the service provider, but based on the user’s perception.

Human Resources quality can moderate the relationship between the information quality and user satisfaction of Accrual-Based Accounting System of Institutions application in the service partner work units of Indonesia Government. The Human Resources function serves as the moderating variable of the relationship between Information Quality and Accurate, accurate, trustable, on time, relevant, understandable and detailed indicators of user satisfaction of the Accrual-Based Accounting System of Institutions application. These results support the Adaptive Behavior Assessment System (ABAS) Theory where Human Resources quality supports moderate the relationship between the information quality and user satisfaction of Accrual-Based Accounting System. Technological development is very rapid, information technology created is increasingly sophisticated, so employees must have broad capabilities and skills. However, not all employees have broad skills and skills so training and human resource development are needed so that their abilities and skills can be used in carrying out organizational activities. A well-organized Human Resource Information System, organizations can get any information related to employees. Management of human resource management is all programs ranging from human resource planning, recruitment, employee development, career development to pension programs can be implemented optimally and on target. Human Resources Information Systems must be designed to provide information. The desired information generally includes timely, accurate, concise, relevant, complete. An effective personnel information system is very helpful for decision making for organizational leaders in good human resource management.

The results of the study can contribute to the knowledge and development of accounting literature, especially public sector accounting, which is related to the interaction of the financial report compilers using applications at the lowest level of the accounting entity. Simultaneously the results of this study are expected to contribute to the government in this case the Ministry of Finance can be feedback, input and can be a reference in making future policies, especially those relating to the development of accounting systems applications that involve many stakeholders.