nueva página del texto (beta)

nueva página del texto (beta) Inglés (pdf)

Inglés (pdf)

Artículo en XML

Artículo en XML Referencias del artículo

Referencias del artículo

Enviar artículo por email

Enviar artículo por email Citado por SciELO

Citado por SciELO  Similares en

SciELO

Similares en

SciELO

Permalink

PermalinkIntroduction

Debt is usually the primary external financing source for large Mexican firms. Historically, these firms have financed long-term projects by issuing public debt through corporate bonds or by private placements with financial institutions such as traditional bank loans or leasing agreements. During the 90s, Mexico witnessed an increase in the demand for a new kind of debt instrument, the syndicated loan. This growth was fostered by the increasing competition in the financial sector by non-banking institutions, the merging and acquisitions in the sector, and the development of secondary credit markets. According to the Global Financial Development Database of the World Bank, in Mexico, syndicated loans represented around 4.11% of the GDP in 2019. Regardless of the relative importance of this type of credit, its role as one of the financing alternatives of Mexican firms is still very limited (Altunbaş et al. (2010)).

A syndicated loan is a contract where at least two creditors join to provide funds for a single borrower. Legally, each syndicate member has a separate agreement with the company, but the terms of each contract are identical for all lenders. The participants of the syndicate agree to share the associated losses proportionally. Unanimity is required to change contract terms such as principal, interest, maturity or collateral. However, renegotiating minor terms, as in case of a technical default on a covenant, requires less than unanimity. Dennis and Mullineaux (2000) describe the syndicated loan as an intermediate form of financing on a continuum of debt instruments. At one end, we have single lender financing such as bank loans or leasing contracts, which are continuously and closely monitored. At the other end, we find public issuance of debt, where direct relationship between investors and the company is weak.

The financial statements of firms show great heterogeneity with respect to the type of debt instruments they use. We can observe a variety of maturities, terms, covenants, and conditions of payment in the contracts (Rauh and Sufi (2010)). The theoretical and empirical literature recognizes this heterogeneity and attempts to explain the choice made by companies between transactional lending (bonds) and relationship lending (traditional bank loans). Three arguments are used to explain the choice between these two categories of financial instruments. The first argument refers to the costs of issuing bonds, which are usually very high. In this case, companies will only use this instrument when the required funds are substantial (Easterwood and Kadapakkam (1991)). The second argument explains that companies with higher ex-ante probability of having financial distress will choose bank loans. This choice is because the renegotiation and/or possible liquidation becomes more difficult as the number of creditors increases. In addition, investors of corporate bonds cannot distinguish between projects worth continuing and those that optimally should be liquidated. This information asymmetry induce strong covenants in the bond contracts, which could cause premature liquidations of profitable projects (Chemmanur and Fulghieri (1994), Detragiache (1994)). The third argument is based in the pecking order theory (Myers and Majluf (1984)). It states that companies choose their debt structure depending on the degree of asymmetric information between creditors and the firm. A firm supports high contracting costs in the bond market because creditors cannot monitor their activities. Banks are more efficient and effective monitors in this case. Some authors state that companies move from bank debt to public debt as the credit quality of the company increases (Diamond (1991), Bolton and Freixas (2000)).

The empirical literature supports the previous theoretical arguments. Denis and Mihov (2003) show that companies with a higher credit rating issue public debt, middle-graded firms borrow from banks, and low-graded firms prefer non-bank creditors. Yosha (1995) shows that firms with growth opportunities linked to their R&D prefer bank bonds to avoid disseminating private information to competitors. Several studies found that the probability of issuing public debt is positively related to firm size and leverage level (Hadlock and James (2002), Cantillo and Wright (2000)). The evidence is mixed when it comes to growth opportunities. Cantillo and Wright (2000) document a positive relationship between growth opportunities and the use of private debt. However, Houston and James (1996) reported a negative relationship for companies that maintain relations with only one bank. Morellec et al. (2015) present evidence that firms with more growth options, higher bargaining power in default, operating in more competitive markets and facing lower credit supply, are more likely to issue bonds.

The evolution of syndicated loans and corporate bonds has been exposed to macroeconomic shocks and several and recent papers have documented such impacts (Mattes et al. (2013), Goel and Garralda (2020), Berg et al. (2021), Hasan et al. (2021), Takaoka and Takahashi (2022)). However, the empirical studies that addresses the choice and relationship between different multi lender long-term debt are scarce and mainly centered in the differences in pricing of the two types of contracts (Angbazo et al. (1998), Santos and Winton (2008)). Furthermore, in these studies authors use data from American, European and Asian companies (see Maskara and Mullineaux (2011), Altunbaş et al. (2010), and Esho et al. (2001), respectively).

With this paper, we extend the literature on the choice of companies between public debt and syndicated loans for an emerging country like Mexico. With a novel and hand-collected dataset, we provide evidence of the role of credit quality, firm size, and the fixed assets to total assets ratio in choosing between the two sources of debt. As another novelty for this type of research, we use Multinomial Logistic Regressions. It allows us to identify the average and marginal effects over the range of the key firm characteristics on the choice of debt instrument.

The rest of this paper is organized as follows. The following Section 2 is devoted to the discussion of our hypotheses. The data and the econometric model we used is described in Section 3. In Section 4 we present our empirical results. In Section 5 we discuss our findings. Section 6 we give our final conclusions.

Factors affecting the long term corporate debt choice

Corporate bonds and syndicated loans have become key sources of new external finance for firms in both developing and developed countries. The annual amount of debt financing raised in these markets increased more than 6-fold from 1991 to 2014 when it reached 5.1 trillion or about 7% of the world gross product (Cortina et al. (2018)). Figure 1 shows the evolution of the two types of debt in Mexico, according to the Global Financial Development Database of the World Bank. In Mexico, the 2008 financial crisis and the COVID pandemia reduced both types of lending but it seems that crisis affect more syndicated loans. It is clear that the two sources of funding are substitutes: one increases at the expense of the other.

Source: Prepared by the authors on the basis of data supplied by the Global Financial Development Database of the World Bank 2022.

Figure 1 Evolution of the two types of debt in Mexico.

In this section we present the hypotheses that explain the choice between raising funds in the syndicated loan market or raising them directly via the corporate bond market. We focus on the financial characteristics of firms related to factors such as the renegotiation and liquidation, information asymmetries and transaction costs.

Asymmetric information and agency costs

The asymmetric information and agency costs hypothesis tells us that opaque companies, i.e. those that are more difficult to monitor, will prefer private over public debt. The literature on agency costs related to debt financing emphasizes that banks are intermediaries that provide monitoring services efficiently (Diamond (1991)). To reduce the moral hazard problem, creditors demand more restrictive clauses and better collateral. Firms with high values of tangible assets can offer these assets as collateral. We hypothesize that those companies with enough collateralizable assets should prefer syndicated loans over bonds. Therefore, all else equal:

H1. As the percentage of tangible assets increases it is more likely to sign a syndicated loan and less likely to issue a public bond.

Flotation costs

The flotation costs hypothesis tells us that public debt issued in domestic markets often involves high flotation costs in the form of registration fees and legal and accounting costs. Firms likely use economies of scale to try to mitigate this fixed cost component by issuing a high number of bonds (Johnson (1997)). On the other hand, the issuance of private debt avoids many of these costs. It is then expected the issuance of public debt to be positively related to firm size. If the same argument is applied to syndicated loans, the probability of issuing a syndicated loan increases if the company is small. The small size limits the firm ability to raise funds in the public market since the high fixed costs make the bond issuance not feasible. We posit the following hypotheses:

H2. As the size of the firm increases, it is more likely to issue public bonds and less likely to issue a syndicated loan.

Renegotiation and liquidation

The renegotiation and liquidation hypothesis argues that companies with a high ex-ante likelihood of financial distress are less likely to issue public corporate bonds. This is because renegotiation in default is very difficult when there are many creditors (Chemmanur and Fulghieri (1994)). Previous empirical evidence suggests a positive relationship between the issuance of public debt and the proxies for the credit quality of companies (Cantillo and Wright (2000), Denis and Mihov (2003), Esho et al. (2001), Roberts and Sufi (2009), Roberts (2015), Demiroglu and James (2015)). In a syndicated loan the number of creditors is much lower than the number of investors of a corporate bond. Therefore, we expect that syndicated loans be preferred by companies with poor credit quality. All else equal:

H3) As the credit quality of the firm increases it is more likely to issue a public bond and less likely to sign a syndicated loan.

Data and methodology

Data

Our sample includes information from Mexican companies listed on the Mexican Stock Exchange (Bolsa Mexicana de Valores, BMV) and covers the period from 2004 to 2011. This period corresponds to an expansion-recession economic cycle (Calderón and Hernández (2017)).

To test our hypotheses, we hand collected information directly from the annual reports of the listed companies and combined it with information provided by Capital IQ. We excluded financial firms and those who did not have all the annual reports in the considered period. Given these constraints, the sample is composed of 79 companies. The frequency of all our data is annual.

We used data on incremental financing decisions based on the analysis of the financial statements of our sample of Mexican companies. From annual financial reports we were able to extract information on relevant loans that the firm holds, or that were signed on the fiscal year. This incremental approach has been used by Hovakimian et al. (2001) to study the choice between equity and debt, by Jung et al. (1996) to analyze the decision to use external funding or not, and by Guedes and Opler (1996) to study the determinants of the maturity of the debt instruments of firms. We used the annual financial reports instead of the balance sheets, because in this second source debt is usually aggregated. This makes impossible to distinguish between private and public debt, or between bank and non-bank debt. Balance sheets give us information about time averaged financing decisions, which can lead to measurement errors and bias in the results (Houston and James (1996) and Johnson (1997)). Using the information from the annual reports allows us to focus on the choice of firms between issuing domestic bonds and the signing of a syndicated loan contract. Notice that these two instruments perform similar functions. We argue that syndicated loans are the only financing alternative to issuing corporate bonds for large firms, in terms of the size and maturity of the funds they provide.

Table 1 presents summary statistics of our sample. Synd is a dichotomous variable that takes the value 1 if the firm issued a syndicated loan during that fiscal year, and 0 otherwise. Analogously, Cebur is 1 if the firm issued a public bond during that year, and 0 otherwise. It must be said that we only considered domestic bonds (in Mexico they are called Certificado Bursátil, or Cebur). We do not have information on bond issues in international markets.

Table 1 Descriptive statistics per variable per year.

| Obs | Mean | Std | Skewness | Kurtosis | min | Median | max | |

|---|---|---|---|---|---|---|---|---|

| Synd | 627 | 0.090 | 0.290 | 2.780 | 8.730 | 0 | 0.000 | 1 |

| Cebur | 626 | 0.110 | 0.320 | 2.440 | 6.940 | 0 | 0.000 | 1 |

| z_score | 577 | 2.700 | 1.850 | 1.430 | 8.290 | -2.470 | 2.510 | 13.000 |

| Tangibility | 623 | 0.410 | 0.220 | -0.260 | 2.120 | 0.000 | 0.440 | 0.940 |

| log_assets | 624 | 4.090 | 0.690 | -0.240 | 3.070 | 2.250 | 4.150 | 5.980 |

| revenue_growth | 622 | 0.110 | 0.240 | 2.020 | 19.650 | -1.000 | 0.100 | 2.240 |

| Solvency | 574 | 7.500 | 67.970 | 11.490 | 140.860 | -18.310 | 0.280 | 966.720 |

| ROA | 619 | 0.060 | 0.050 | 0.750 | 7.320 | -0.120 | 0.050 | 0.350 |

| Internationalization | 444 | 0.570 | 0.500 | -0.270 | 1.070 | 0 | 1.000 | 1 |

Source: Prepared by the authors

We constructed the dependent categorical variable debt_type that can only take the values O, S, or C. For any given fiscal year, firms that did not issue new debt of any of the two types we are studying, domestic public bonds and syndicated loans, were classified in category O (i.e., when synd=cebur=0). Firms that issued a syndicated loan but did not issue a public bond were classified in category S (synd=1, cebur=0). Finally, firms that issued a public bond and did not issue a syndicated loan were classified in category C (synd=0, cebur=1). We decided to omit a possible fourth category (synd=cebur=1) because in our sample there are only 5 observations out of 631 where the firm issued both types of debt, in the period considered. This reinforces our assumptions that corporate bonds and syndicated loans are substitutes for long-term funding.

An important control variable that is not showed in Table 1 is Sector, the economic sector of the company. We use the North American Industry Classification System (NAICS). In our sample there are no firms from Sector 1 (Agriculture, Forestry, Fishing and Hunting). Sector 2, where 14.1% of our sample lies, consists of companies engaged in Mining, Quarrying, Oil and Gas Extraction, Utilities and Construction. Most of the companies in our sample (46.2%) are classified in Sector 3, the Manufacturing sector. This is followed by companies in the Sector 4 (with 20.5%), which consist of firms engaged in Wholesale Trade, Retail Trade, Transportation, and Warehousing. In Sector 5 (with 10.3%) we have Telecommunications and Information companies. Financial companies also belong to this sector, but we excluded them from our study. Finally, we grouped sectors 6 and 7 into one since they account together for 9% of our firms. This new Sector 6_7 includes various activities such as Educational Services, Health Care, Social Assistance, Entertainment, Recreation, Accommodation, and Food Services. Table 2 shows the complete list of firms in our sample.

Table 2 Economic sectors following NAICS

| Sector 2 | Sector 3 | Sector 4 | Sector 5 | Sector 6 | Sector 7 |

|---|---|---|---|---|---|

| ara, autlan, geo, gmexico, hogar, homex, ica, peñoles, ruba, sare, urbi |

ahmsa , bachoco, bafar, bimbo, cemex, ceramic, cmoctez, codusa, collado, conver, copamex, cydasa, edoardo, ekco, femsa, gcarso, gcc, gissa, gmacma, gmd, gmodern, gruma, herdez, hilasal, ich, kimber, kof, lamosa, mexichem, minsa, nemak, sanluis, sigma, tekchem, vitro, xignux |

accelsa, almaco, asur, bevides, comerci, elektra, ferromx, fragua, gfamsa, gigante, gmarti, gph, livepol, sab, soriana, tmm, walmex |

amx, axtel, cable, pasa, rcentro, telmex, tlvisa, tvazteca |

cnci, medica |

alsea, cidmega, cie, cmr, posadas |

Source: Prepared by the authors.

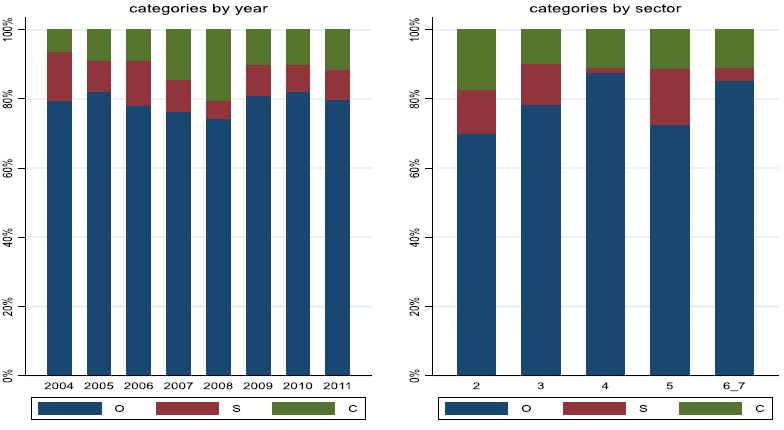

As we employ year and sector variables as controls in our models, in Figure 2 we show the distribution of the dependent variable per year and sector.

Source: Prepared by the authors.

Figure 2 Distribution of the three categories of credit per year and sector.

As we can see, in the studied period, most companies did not issue neither long-term debt nor syndicated loans. The maximum percentage of companies that obtained a new syndicated loan in one given year does not exceed 15%. The evolution of the percentage of companies that issued public debt shows the impact of the financial crisis of 2008 in the debt markets. The increasing trend in the use of this instrument is broken in 2008 and not recovered until 2011. The sector with a higher percentage of companies issuing syndicated loans is the Sector 5 (Telecommunications and Information firms). The issuance of public bonds peaks in Sector 2 (Mining, Quarrying, Oil and Gas Extraction, Utilities and Construction firms).

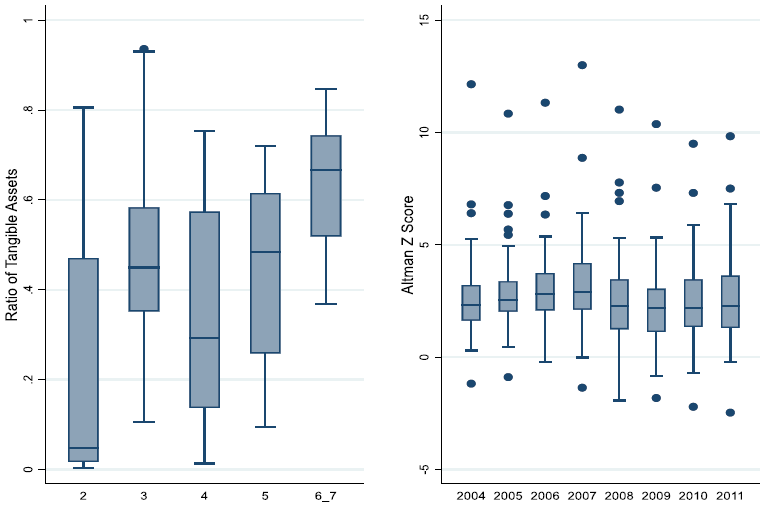

Variables z_score, tangibility, and log_assets, will be used to describe the main features of each company. Our first explanatory variable, z_score is the Altman’s Z-score provided by Capital IQ and serves as a proxy for the company's credit quality. Altman’s Z-score model has been widely employed for measuring bankruptcy risk and has also been tested in multiple studies (Balcaen and Ooghe (2006), Bauer and Agarval (2014), Grice and Ingram (2001), Kumar and Ravi (2007)), and across different markets such as China (Wang and Campbell (2010)), India (Singh and Singla (2019)), Vietnam (Tung and Phung (2019)), Japan (Xu and Zhang (2009)), Turkey (Cindik and Armutlulu (2021)), Europe (Altman et al. (2017)) and USA (Li and Rahgozar (2012), Chiaramonte et al. (2016)). In the case of Mexico, Chávez and Hernandez (2018) applied the Z-score as the evaluation standard to analyze and predict the financial status of small and medium enterprises from Tuxtepec, Oaxaca, in Mexico. More recently, Pantoja-Aguilar et al. (2021) used the Z-score to analyze the Mexican firms' risk in the Bolsa Mexicana de Valores.

Figure 3 shows the evolution of the Z-score in our sample of Mexican firms during the considered period. The upward trend in the average credit quality of firms suffers a noticeably break in the 2008.

The variable tangibility is our proxy for the percentage of the collateralizable assets and is defined as the ratio between the value of tangible assets and total assets of a company. In our sample, tangible assets represent on average about 40% of total assets. Interestingly, this average declines in the period considered. As this financial ratio presents a different behavior by industry and is one of the characteristics that distinguishes each sector, Figure 3 shows its distribution by sector. The literature on debt structure uses tangibility as a proxy for liquidation costs. Asset tangibility may reduce information asymmetries because tangible assets are more easily evaluated by corporate outsiders than intangible assets such as R&D expenses (Roberts and Sufi (2009), Colla et al. (2013)).

Regarding the size of the companies, their average total assets (before taking logarithm) is between 9,082 and 16,430 million of Mexican pesos. Our log_assets is the base 10 logarithm of the total firm assets. The behavior of log_assets in Table 1 shows that during the period 2004-2011 the mean of this variable has increased, and also its dispersion.

We include in our estimated model several control variables that have been shown to affect debt structure (Denis and Mihov (2003), Erel et al. (2012), Gomes and Philips (2012), Colla et al. (2013). As control variables we use revenue_growth, long term solvency, ROA, Internationalization, Sector and Year. Revenue growth is used as a proxy of growth options (Whited (2006), Grullon et al. (2012), Morellec et al. (2015)) and is defined as the revenue growth rate over the previous year. solvency is a proxy for long term solvency of the firm and is computed as the ratio of EBITDA minus Capital Expenditure over Total Debt (Roberts and Sufi (2009)). ROA is the Return on Assets, provided by Capital IQ. Internationalization is a dichotomous variable that takes the value 1 if the firm operates in foreign markets, and 0 otherwise. Our model includes Year fixed effects, which serves as proxy for macroeconomic and financial environment.

Methodology

We use the Multinomial Logistic Regression (or simply Multinomial Logit) to test our hypotheses ob the determinants of the choice of companies on the type of long-term debt issued. Denote by:

and by

where:

Given that

It is important to mention that even though the previous equations depend on the base category chosen, the final values of

We can algebraically differentiate equations (2) with respect to each independent variable in order to obtain the marginal effect

Notice that:

Using (1), and ignoring the control dummies for clarity, we obtain that:

By analyzing the signs of difference of the coefficients

Results

With the panel data described in Section 3, we estimated the Multinomial Logit Model described in the previous section. To test for robustness, we estimated both Logit and Probit regression models. We also estimated the simple univariate versions of the Logit and Probit models. In that case we estimated two separate regressions, one for categories O and S, and the other for categories O and C. All our results were qualitatively consistent across models, with minor variations in the values of the estimations. For this reason we decided to present here only the results from the Multinomial Logit Model.

We show the coefficient estimates from the Multinomial Logit Model in Table 3 panel A. Because we chose category O as the base outcome, we estimate for each year the log-odds ratio of issuing a syndicated credit or a public bond, relative to not issuing any of the two. Additionally, in order to capture potential nonlinear effects in credit quality, a quadratic variable was added in the Altman’s Z-score. In panel A the coefficient estimates of the control variable year are not reported due to the lack of statistical significance.

Table 3 Panel A. Estimated coefficients of the Multinomial Logit Model (with category O as the base outcome). Panel B. Unilateral tests of hypotheses for the difference of the estimated coefficients.

| panel A | panel B | |||

|---|---|---|---|---|

| estimated coefficients | difference of estimated coefficients |

Alternative Hypothesis tested |

||

| S | C | |||

| z_score | 2.111*** | 0.729 | 1.382* | > 0 |

| (2.81) | (1.21) | |||

| z_score2 | -0.425*** | -0.189* | -0.236* | < 0 |

| (-2.81) | (-1.70) | |||

| Tangibility | 2.731** | -3.805*** | 6.535*** | > 0 |

| (2.39) | (-2.95) | |||

| log_assets | 1.341*** | 2.274*** | -0.932** | < 0 |

| (3.79) | (4.81) | |||

| revenue_growth | 0.301 | 0.851 | ||

| (0.31) | (0.76) | |||

| Solvency | -0.103 | -0.113 | ||

| (-0.69) | (-0.65) | |||

| ROA | -5.584 | 17.087** | ||

| (-0.83) | (2.55) | |||

| Internacionalization | 0.388 | -1.085** | ||

| (0.77) | (-2.13) | |||

| Sector (base=Sector 2) | ||||

| 3 | -1.563*** | 0.803 | ||

| (-2.59) | (1.17) | |||

| 4 | -3.484*** | 0.276 | ||

| (-3.57) | (0.40) | |||

| 5 | -1.273 | -0.836 | ||

| (-1.61) | (-0.78) | |||

| 6_7 | -2.456** | 3.257*** | ||

| (-2.44) | (3.20) | |||

| Constant | -8.497*** | -12.77*** | 4.272* | > 0 |

| (-4.65) | (-5.44) | |||

| No. observations: | 376 | |||

| McFadden R2: | 0.248 | |||

| adjusted McFadden R2: | 0.101 | |||

| Cox & Snell R2: | 0.301 | |||

| Cragg-Uhler/Nagelkerke R2: | 0.394 | |||

* p< 0.05, ** p <0.01, *** p <0.001, t-statistics in parentheses

Source: Prepared by the authors.

Table 3 panel A shows that relative to the base category O, the odds ratio of issuing a syndicated loan increases as the credit risk becomes smaller (higher Z-score). Also, the Z-score effect is potentially non-linear as shown by the significantly negative coefficient estimates of the quadratic term. This would mean that the effect of the credit quality could have an increasing-decreasing impact on the decision. That is, at certain level of Z-score there is a maximum odds ratio of issuance relative to no issuance, conditional on other observable variables of the company. In terms of firm size, companies with a higher value of assets significantly increase their odds ratio of issuing both types of debt. However, the tangibility of those assets has opposite effects for the two debt types. Companies with higher levels of tangibility are more likely to issue syndicated loans but less likely to issue corporate bonds, relative to the base category.

The direct interpretation of the actual values of the estimated coefficients as marginal effects could be misleading for two main reasons. First, all the effects described are relative to the base category chosen. Second, they are in terms of log-odds instead of actual probabilities. The introduction of the quadratic term in z_score makes this interpretation even harder. In what follows, we discuss the marginal effects of each variable on the probability of issuing both types of debt. These effects are absolute in the sense that they are independent of the base category chosen for the calibration of the Multinomial Logit Model.

Table 4 shows the estimated average marginal effects. As we can see, an increase of one unit on the Z-score increases the probability of choosing a syndicated loan by 1.55%, and reduces the probability of choosing a corporate bond by 1.73%, on average. These values already take into account the quadratic effect of the variable. However, both numbers are not statistically significant. This lack of significance is a consequence of averaging over the whole range of values of z_score, where the effect takes both signs. We will regain significance by computing the marginal effect at specific values of the variable.

Table 4 Average marginal effects on the probability of issuance of both types of debt. dy/dx for factor levels is the discrete change from the base level.

| dy/dx | ||

|---|---|---|

| X | y = Pr(S) | y = Pr(C) |

| z_score | 0.0155 | -0.0173 |

| (1.01) | (-1.12) | |

| Tangibility | 0.3007*** | -0.3476*** |

| (3.13) | (-3.53) | |

| log_assets | 0.0865*** | 0.1638*** |

| (3.05) | (4.65) | |

| Sector (base = Sector 2) | ||

| 3 | -0.2344*** | 0.0797** |

| (-2.59) | (2.20) | |

| 4 | -0.3385*** | 0.0549 |

| (-3.77) | (1.43) | |

| 5 | -0.1828 | -0.0159 |

| (-1.64) | (-0.44) | |

| 6_7 | -0.3295*** | 0.3836*** |

| (-3.56) | (4.52) | |

* p <0.05, ** p <0.01, *** p< 0.001, t-statistics in parentheses

Source: Prepared by the authors.

By contrast, the average marginal effect is statistically significant for the other two explanatory variables. For instance, the increase in the tangibility of assets rises the probability of issuing a syndicated loan and reduces the probability of issuing a public bond. For a 10% increase in tangibility, on average, the probability of choosing S increases by 3%, while the probability of choosing C decreases by 3.48%, all other factors held equal.

On the other hand, larger companies are more likely to issue both types of debt. More precisely, all else being equal, if the size of the company increases by 10 times (an increase of one unit on log_assets), the probability of choosing the category S increases by 8.65% on average. Similarly, the probability of choosing category C increases on average by 16.38%.

Regarding the economic sector we can assert that, on average, firms in sectors 3, 4, 6 and 7 issue syndicated loans with significantly less frequency than those in sector 2, assuming all other characteristics are similar. In the same way, firms in sectors 3, 6 and 7 are significantly more likely to issue public bonds than those in sector 2.

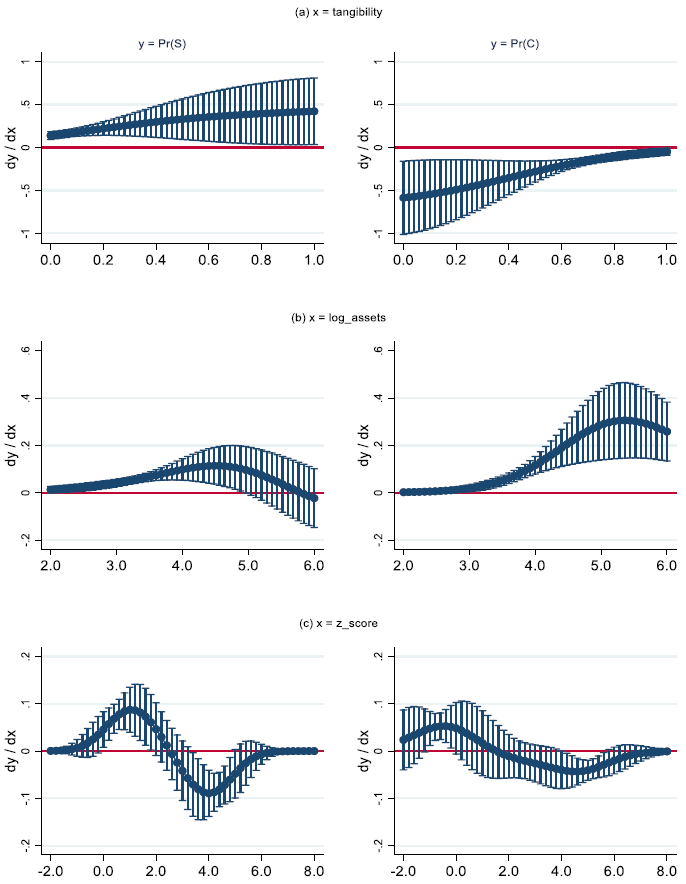

It is important to emphasize that all effects described above are the average for all the firm-year observations in the sample. Average marginal effects computed in this way do not allow us to discern whether these effects are uniform throughout the whole range of values taken by the independent variables considered. For instance, Table 3 shows signs of potentially non-monotonic effects of the credit quality on the probability of issuance of both types of debt. For this reason, we will now consider one explanatory variable at a time, and for each possible value of that variable, we will compute the marginal effects averaging on the remaining variables. Figure 4 shows that the effects are not uniform in intensity, and in some cases not even in sign, over the entire range of values of each variable.

Source: Prepared by the authors.

Figure 4 Average marginal effects on the probability of issuance of both types of debt at different levels of tangibility, log_assets and z_score.

Figure 4(a) depicts how the average marginal effects of tangibility on the probability of issuance of both types of debt change over the whole range of the variable. As we can see, for all possible values of tangibility, the effect is significantly positive for category S, and significantly negative for category C. This result implies that the increase in the tangibility of assets rises the probability of signing a syndicated loan, and reduces the probability of issuing a public bond. We already predicted this with Table 4, but now we have more information. For instance, we can see that the marginal effect is more substantial for syndicated loans at high levels of tangibility. It is also stronger at low levels of this variable for public bonds.

The left side of Figure 4(a) confirms the first assertion in our hypothesis H1 about asymmetric information and agency costs. A firm with better collateral is on average more likely to issue a syndicated loan, and this effect increases with the value of our proxy variable. The right side of Figure 4(a) complements the reasoning, showing a clear preference for the issuance of public debt for companies with worst collateral.

Figure 4(b) shows that the average marginal effect of log_assets is positive for both categories over the whole range of firm sizes, although it is not statistically significant for the biggest firms in the S category. This implies that as the size of the firm increases, the probability of issuing both types of debt also increases. Our hypothesis H2 about flotation costs is confirmed by this figure.

The analysis is slightly more complex in the case of z_score variable. Figure 4(c) shows the average marginal effect of Z-score for the range of values between -2 and 8, where the majority of our observations lay. Here we visualize how the quadratic effect on creditworthiness effectively plays an important role in the probability of choosing the type of debt, and the sign of this effect changes depending on the range of Z-score. Roughly around the gray zone (that Altman defines form 1.81 to 2.99) we cannot statistically distinguish the average marginal effect from zero. For the smallest values of z_score the average marginal effect is significantly positive, which means that the probability of issuing debt increases with the creditworthiness. For the largest values of z_score the average marginal effect is significantly negative, so the probability of issuing debt decreases. All his implies that there is a value of z_score in this range were the probability of issuing a syndicated loan attain its maximum. The same phenomenon occurs for the public bonds issues, although the maximum in not necessarily attained at the same value of the variable.

Loosely speaking, the probability of issuing both types of debt increases for companies in the risky zone, it is at is maximum inside the gray zone, and then decreases for companies in the safe zone. These empirical results confirms our hypothesis H3 about renegotiation and settlement for the riskiest companies, but contradicts it for the safest ones.

All the previous analysis gives us information about the behavior under different scenarios of the probability of issuing each type of debts individually, but nor the relationship between those two probabilities. In order to compare the two probabilities, Table 3 Panel B shows the results of unilateral tests of hypotheses for the difference of the estimated coefficients from Table 3 Panel A. As we can see, we can accept all the alternatives hypotheses:

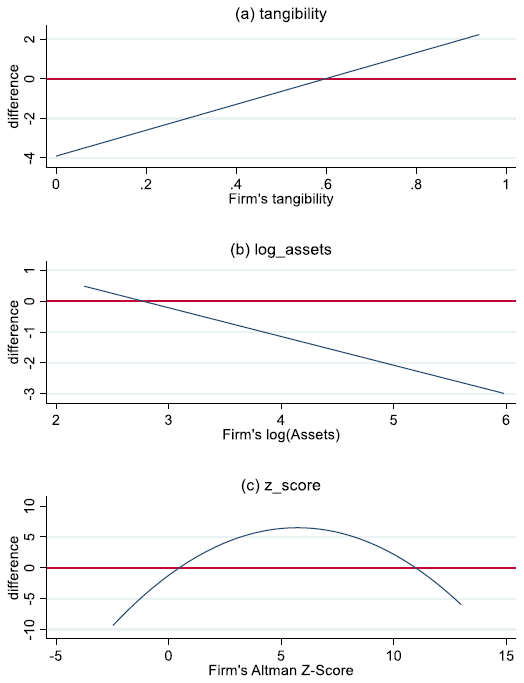

In Figure 5 we plot the differences of scores as shown in equation (3). For example, in Figure 5(a) we hold all variables at their average, and only change tangibility. As

Source: Prepared by the authors.

Figure 5 Difference of scores that explains which types of debt has higher probability. The probability of syndication is the highest when the difference is positive, while the probability of emitting a Cebur is the highest when the difference is negative.

Figure 5(a) illustrates that on average, firms with low values of tangibility are more likely to issue public bonds, whereas firms with high values of tangibility are more likely to issue syndicated loans. This seems to support our hypothesis H1 about asymmetric information and agency costs. In Figure 5(b) we see that, on average, large firms prefer public bonds over syndicated loans. This confirms our hypothesis H2 about flotation costs. Finally, Figure 5(c) shows that if the firm is good enough or bad enough, the issuing public bonds will be more likely than the issuance of a syndicated loan. This is consistent with our hypothesis H3 about renegotiation and settlement for good firms, but contradicts H3 for bad firms.

Discussion

This paper provides the first study analyzing the choice of companies between issuing public debt or signing a syndicated loan. Our research belongs to the literature on debt structure, which is a central element in a firm's capital structure. This line of research studies the use of different types of debt such as loans, bonds, credit lines, commercial papers, and leases. Previous literature has studied the coevolution of bonds and syndicated loans but has ignored the factors that determine the choice between one or the other. Also, the literature has analyzed the choice between bonds and single lender bank loans (Houston and James (1996), Johnson (1997), Morellec et al. (2015)). However, we argue that a syndicated loan is a more comparable contract to a bond because multiple lenders are involved. Our analysis is based on a sample of Mexican firms. In related studies, the capital structure of Mexican firms has been addressed in Carmen and Bolívar (2012), Carmen et al. (2015) and García et al. (2012).

The selection of a long-term debt instrument reflects both the needs and context of the firm. Our work in particular shows that the choice between a syndicated loan and a public bond is significantly related to firm characteristics such as credit quality, size, tangibility, and the economic sector in which it operates.

Additionally, our work suggests that the average effects do not capture relevant information on the impact of the variables associated with the company. In the case of credit quality, this variable does not have a uniform sign along its entire range. The marginal effect on the probability of issuing syndicated loan is initially positive and significant for low values of Z-score, and then is negative and significant for higher values. In other words, we found a significant quadratic effect of the firm credit quality on the probability of issuing any of these two types of debt. This non-monotonic effect is more subtle than the previous findings in the literature (Cantillo and Wright (2000), Denis and Mihov (2003), Esho et al. (2001), Roberts and Sufi (2009), Demiroglu and James (2015)), and we believe that it is one of our main original contributions.

We also found that as the size of the firm increases, it is more likely to issue both types of debt, with the largest firms preferring public bonds over syndicated loans. Also, on average, small firms prefer syndicated loans over public bonds. All this is explained by our hypothesis about flotation costs. These results are also found in Houston and James (1996) and Johnson (1997).

Also, in line with our asymmetric information and agency costs hypothesis, we found that as the percentage of tangible assets increases, the firm is more likely to sign a syndicated loan. Furthermore, on average, firms with a very high percentage of tangibility prefer this instrument over the issuance of public bonds. These results are reversed for firms with a low percentage of tangible assets.

Finally, we found much weaker support for our hypothesis about renegotiation and settlement. This negative result is because there seems to be a non-monotonic behavior in the creditworthiness of the firm. More specifically, we found that the likelihood of issuing two types of debt increases for companies in the risky zone, it is at is maximum inside the gray zone, and then decreases for companies in the safe zone. If the firm is either too risky or too safe, the issuance of public bonds will be more likely than the issuance of a syndicated loan.

Conclusions

Optimal debt mix is crucial when determining a firm’s capital structure. This paper studies the determinants of a firm’s debt choice between issuing corporate bonds and a syndicated loan. For this purpose, we go beyond the study of average effects and analyze the marginal contribution of capital structure determinants over debt choice.

This research provides evidence of the nonlinear effects of credit quality on the choice between syndicated loans and bonds and contributes to the literature on debt structure

Prior studies on the use of different types of debt focus mainly on the choice between traditional sole-lender bank debt versus publicly issued bonds. We extend the debt specialization literature by incorporating the study of marginal effects of determinants, such as firms´ size and risk, over the debt mix and selecting traditional methods of corporate bonds against more complex instruments, such as syndicated loans.

In particular, we show that a firm with better collateral is on average, more likely to issue a syndicated loan, and this effect increases with the value of our proxy variable. This particular results confirm the hypothesis of asymmetric information and agency costs

On the other hand, the average marginal effect of size is positive for both categories over the whole range of firm sizes. However, it is not statistically significant for the biggest firms in the syndicated loan category. This finding implies that as the size of the firm increases, the probability of issuing both types of debt also increases, confirming the hypothesis about flotation costs.

Finally, the marginal effect of risk over the probability of issuing both types of debt is nonlinear: it increases for companies in the risky zone, it is at its maximum inside a gray zone, and then decreases for companies in the safe zone. These empirical results confirm our hypothesis on renegotiation and settlement for the riskiest companies but contradict it for the safest ones.

Therefore, our results contributes to literature by showing how collateralization (as measured by tangibility), size (as measured by assets), and risk (defined by Altman’s Z-score) are fundamental factors that non-linearly explain the choice between two debt instruments that are substitutes, and indirectly, debt level and optimal capital structure.

Our findings are similar to those in Morellec et al. (2015). They model the choice between bonds and bank loans and show that firms facing high growth opportunities, higher bargaining power in default, operating in more competitive product markets and facing lower credit supply are more likely to issue public debt.

A final contribution is to extend the scope of the debt specialization literature to non-Anglo-American contexts. Our study might enable scholars to explore the peculiarities of a wider set of national environments emphasizing how they can affect IPOs.

Limitations and further research

One limitation of our work is the size of our sample and type of information provided by Capital IQ. Using different measures for credit quality such as debt ratings could yield more detailed and focused results, but this kind of information is lacking for public Mexican firms. We also acknowledge that the change in accounting standards that occurred in Mexico in 2009 could have an impact1.

We note that we have no information about the issuance of public debt by firms in our sample in foreign markets. This information would have considerably enriched the conclusions of our work.

We consider that the specific subject that we study is clearly influenced by the economic cycle. It would be interesting to expand the sample period in further research. In particular, it is important to explore structural changes in the decision-making process of the firms.