Servicios Personalizados

Revista

Articulo

texto en

texto en  Inglés (pdf)

Inglés (pdf)

Artículo en XML

Artículo en XML Referencias del artículo

Referencias del artículo

Enviar artículo por email

Enviar artículo por emailIndicadores

-

Citado por SciELO

Citado por SciELO -

Accesos

Accesos

Links relacionados

-

Similares en

SciELO

Similares en

SciELO

Compartir

Permalink

PermalinkContaduría y administración

versión impresa ISSN 0186-1042

Contad. Adm vol.68 no.1 Ciudad de México ene./mar. 2023 Epub 14-Ene-2025

https://doi.org/10.22201/fca.24488410e.2023.4810

Articles

Cash level determinants in a group of Mexican Stock Exchange issuers

1 Universidad Juárez del Estado de Durango, México

2 Universidad Autónoma del Estado de Quintana Roo, México

Based on Keynes's arguments on the functions of money, short-term financial decisions, especially the level of cash, are of interest due to their impact on the financial performance of companies and the expectations of various economic agents. Previous evidence suggests that the level of cash depends on endogenous and exogenous aspects. Within the latter, the Covid-19 pandemic would fit due to its effect on business dynamics. This study offers an analysis of the behavior of cash levels in a sample of 29 issuers listed on the Mexican Stock Exchange based on a series of proposed determinants, evaluating the pandemic's effect on such a relationship. Using a panel data model, we studied the period between 1T2001 and 1T2022. The main results of the analysis show that the uncertainty, flow, and size of the companies are the factors with the most significant direct impact on the level of cash. At the same time, the relationship is inverse for leverage, investment in fixed assets, and capital market behavior. The results have implications for the investment and financing decisions of administrators, investors, and regulators.

JEL Code: M10; M41; G39

Keywords: cash holdings; Mexican Stock Exchange; macroeconomic risk

Desde los argumentos de Keynes sobre las funciones del dinero, las decisiones financieras de corto plazo, en especial el nivel de efectivo, es de interés por su impacto en el desempeño financiero de las empresas y en las expectativas de diversos agentes económicos. Evidencia previa sugiere que el nivel de efectivo depende de aspectos endógenos y exógenos, dentro de estos últimos cabría la pandemia por Covid-19, por su efecto en la dinámica empresarial. El presente estudio ofrece un análisis del comportamiento de los niveles de efectivo en una muestra de 29 emisoras que cotizan en la Bolsa Mexicana de Valores a partir de una serie de determinantes propuestos, evaluando el efecto que tuvo la pandemia en tal relación. Mediante un modelo para datos en panel se estudia el periodo entre el 1T2001 y el 1T2022. Los principales resultados del análisis realizado demuestran que la incertidumbre, el flujo y tamaño de las empresas son los factores de mayor impacto directo sobre el nivel de efectivo, mientras que la relación es inversa para el apalancamiento, la inversión en activos fijos y el comportamiento del mercado de capitales. Los resultados tienen implicaciones en las decisiones de inversión y financiamiento de administradores, inversionistas y reguladores.

Código JEL: M10; M41; G39

Palabras clave: nivel de efectivo; Bolsa Mexicana de Valores; riesgo macroeconómico

Introduction

Under an inclusive vision, companies aim to generate benefits for all stakeholders through investment and employment, offering quality products and services, and contributing to public finances (payment of taxes), among other aspects. Nevertheless, the current economic-financial paradigm reduces this vision to the creation of shareholder value. Thus, the role of financial managers, in their eagerness to achieve this objective, is to make decisions in three main areas: investment, financing, and dividend policy. Although these decisions affect overall financial performance, it is worth highlighting the importance of short-run decisions, particularly the amount of cash companies keep in their financial structure.

Since Keynes’ pioneering approaches, where he proposed four justifications for holding cash, spending, business, precautionary, and speculative, various efforts have attempted to identify the determinants of the level of cash held by companies (Opler et al., 1999; Almeida et al., 2004; Ferreira & Vitela, 2004; Foley et al., 2007; Yepes & Restrepo, 2016). On the other hand, there is research that relates the level of cash to some financial characteristics, such as the value of the company or its profitability (Pinkowitz & Williamson, 2002; Pinkowitz et al., 2006; Martínez et al., 2013; Harford et al., 2008; Le, 2019). Although some studies maintain that there is an optimal level of cash (Baumol, 1952; Miller & Orr, 1966), empirical evidence indicates that companies, in general, maintain cash levels that do not respond to such optimization criteria; additionally it is necessary to recognize that there have been significant variations in cash levels over time; for example, in the US economy the average cash levels maintained by companies in their balance sheets went from 10.5% in 1980 to 23.2% during 2006 (Bates et al., 2009). Mexican companies have also shown a significant increase in cash levels, particularly between 2001 and 2022, with an increase of 45.4%1.

As a result of the negative health effects and its high transmission capacity, the SARS-COV-2 virus, discovered at the dawn of 2020, caused the World Health Organization (WHO) health authorities to declare a COVID-19 pandemic. In addition to 6 443 306 deaths and 591 683 619 confirmed cases as of August 19, 2022, the health ravages of the pandemic include hospital overcrowding and drug shortages. COVID-19 has also negatively affected international economic dynamics through significant disruptions in international financial markets, reduced production, and disruption of supply chains, among other aspects. The containment and social lockdown measures implemented by the authorities of the different countries caused, in many cases, major declines in economic and financial activity.

This study analyzes the response of the cash level of a group of companies listed on the Mexican Stock Exchange (BMV) to the influence of a group of proposed factors, contrasting this relation with the outbreak of the COVID-19 pandemic. A panel data study analyzes the information of 29 BMV issuers between 1Q2001 and 1Q2022. The results show that the uncertainty, cash flow, and size of the companies analyzed directly and significantly affect the level of cash. In contrast, the level of indebtedness, capital spending—fixed asset investment—and capital market behavior have an indirect effect.

The following section reviews relevant literature on the cash companies decide to keep in their financial structure and the effects of COVID-19 on financial markets. Sections three and four describe the study’s methodological aspects and the analysis results, respectively. Finally, section five outlines future lines of research in addition to the conclusions of the work.

Review of the literature

In his seminal work The General Theory of Employment, Interest and Money, John Maynard Keynes proposes four motives for holding liquid resources: spending, business, speculative, and precautionary. The first two are related to exchange operations; the speculative motive is associated with unexpected changes in economic-financial conditions that affect the company’s performance, such as the price of inputs, interest rates, and exchange rates. In order to explain cash holdings, previous research has focused on business and precautionary motives (Tomohito & Iichiro, 2021).

Keynes’ precautionary explanation is less sensitive to changes in the interest rate since it responds mainly to “the general activity of the economic system and the level of income-money”; it responds to the need to have cash available to face possible contingencies or to take advantage of investment opportunities with positive net present value (Keynes, 1936). Some proposals have suggested the need to extend Keynes’ (1936) definition of the precautionary motive by considering that cash is not only used to face unexpected spending but also to deal with the uncertainty of expected flows so that to the extent that there are high levels of risk in the pattern of revenue and expenditure, there is an increase in the probability that cash will be available to meet the needs of the economy (Keynes, 1936), The precautionary motive should also consider the effect of uncertainty on investment opportunities (Duchin, 2010), and is usually presented in a scenario in which liquidity in financial markets is restricted (Opler et al., 1999).

The precautionary motive to hold cash will exert a greater influence on companies with higher foreign holdings because such investment opportunities are either larger or more volatile than domestic ones (Foley et al., 2007). Similarly, diversified companies have lower cash levels attributable to the precautionary motive due to the absence of perfect correlations between cash flows and investment needs (Duchin, 2010).

Evidence from previous studies indicates that the precautionary motive explains why companies, especially those under financial stress, increase their cash holdings when their internal liquidity is depleted. For example, during the financial crisis triggered by the 2007 subprime mortgage crisis in the United States, financial managers reacted by holding higher levels of cash as access to credit in the capital markets was restricted, and investment opportunities dwindled (Sun & Wang, 2014). In a more recent case, during the Covid-19 crisis, companies needed to assure adequate cash levels to guarantee their operations and maintain a surplus in order to amortize the risk associated with the uncertainty generated in an environment in which creditors adopted more conservative positions (Xiuhong et al., 2020).

The determination of available cash must consider the period between payments and revenues, the structure and organization of the industry, the return on current investments, acquisition costs, and the relative maintenance cost (Bibow, 1995); access to external sources of financing, financial difficulties, asset liquidity, information asymmetry, and the legal environment, among other aspects, must also be considered (Kaplan & Zingales, 1997). In addition, cash tends to reduce volatility in the company’s cash flows, increase discretionality2 (Opler et al., 1999), be a mechanism to finance investments during recession periods (Harford et al., 2003), and increase the possibility of protecting the company from unexpected changes in future cash flows from operations (Acharya et al., 2007), to mention a few.

Previous studies have analyzed the influence of macroeconomic factors on the level of cash held by companies in their financial structure, such as incorporating dummy variables in longitudinal data to capture the effect of such shocks (Luo & Hachiya, 2005; Bigelli & Sánchez, 2012; Yepes & Restrepo, 2016) and identifying the significant influence of business cycles (Almeida et al., 2004). The volatility of macroeconomic conditions—production—has also been associated, inversely, with the level of cash (Baum et al., 2006). Systematic risk is another aspect with a significant influence on cash demand; to the extent that companies show a higher correlation with macroeconomic shocks, they are perceived as riskier and tend to maintain higher levels (Palazzo, 2011). Uncertainty and instability caused by presidential elections and public policy decisions also affect cash levels (Brandon & Youngsuk, 2012).

The level of cash has been linked to the consolidation of domestic markets to the extent that this level guarantees, based on legal, economic, and political conditions, investors’ capital and its corresponding effect on the companies’ cash levels. For example, Dittmar et al. (2003) and Hardford et al. (2008) point to a negative relation, while Huang et al. (2013) and Iskandar and Jia (2014) document a direct relation.

The literature offers three explanations for how financial policy determines the level of cash that companies should hold: a) trade-off, b) financing hierarchy, and c) free cash flows.

Trade-off

Developed by Modigliani and Miller (1958) to explain a company’s financial structure, this postulate establishes that the appropriate cash level should consider marginal costs and benefits. Holding cash represents an opportunity cost compared to investment possibilities in assets with higher profitability but lower liquidity (Ferreira & Vilela, 2004). Companies compare the costs and benefits of financing when deciding how much cash to hold (Opler et al., 1999), including the transaction costs of debt (Foley et al., 2007). It is also important to consider that a financially distressed company cannot venture into all attractive projects, as holding cash is costly because it requires the sacrifice of some valuable investment opportunities (D’Mello et al., 2008). In periods of uncertainty and volatility, companies are expected to increase their cash levels according to the precautionary motive, so they may choose to suspend dividend payments or have the need to sell assets to obtain liquidity.

According to the trade-off hypothesis, smaller, riskier, and more financially distressed companies tend to hold larger amounts of cash than larger ones (13.2% versus 7.5% of total assets) (Bigelli & Sanchez, 2012).

Funding hierarchy or pecking order

In order to reduce the costs generated by information asymmetry and other costs derived from financing, Myers and Majluf (1984) claim that companies will prefer to finance investment projects with their resources from retained earnings. Once this source is exhausted, they will explore the possibility of contracting debt, and as a last resort, they will opt for equity issuance. Proponents of the pecking order approach argue that information asymmetry prevents determining an optimal amount of cash, so companies use internally generated cash before seeking external resources. Companies with greater investment opportunities should keep as much cash as possible, especially those facing greater challenges in obtaining external financing (Chen & Chuang, 2009).

Free cash flows -FCF-

This approach considers that an economic agent accumulates liquid assets and uses them in its interest, causing, in some cases, detriment to the principal (Weidemann, 2018) since the availability of liquid assets increases managers’ discretion in decision-making and the potential for agency conflicts (Jensen & Meckling, 1976). Based on FCF theory, the impact of agency conflicts on the cash levels of companies has been studied through aspects such as i) the characteristics of the board of directors—a board with greater authority and independence reduces such agency conflicts—(Kusnadi, 2011); ii) the ownership structure is directly associated with cash levels (Ozkan & Ozkan, 2004; Kuan et al., 2011). Moreover, CEOs descended from company founders tend to hold higher cash levels than the succeeding generation (Steijvers & Niskaenen, 2013); iii) the degree of managerial ownership has also been linked as a determinant of cash levels. Nevertheless, the empirical evidence is inconclusive.

Covid-19 and the financial markets

The COVID-19 disease caused by the SARS-CoV-2 virus spread rapidly throughout the world due to its high infection and mortality rates (Sahai et al., 2020), leading WHO authorities to declare a pandemic in March 2020. In the health field, the ravages caused by the disease are almost 6.5 million deaths and 600 million cases confirmed by health authorities as of September 2022. In addition, the containment strategies adopted by the governments facing the COVID-19 pandemic triggered negative effects in the economic and financial field, for example, significant increases in unemployment rates and poverty levels, damage to supply chains, sharp declines in stock markets (Ali et al., 2020), increased financial asset price volatility (Baker et al., 2020; Zhang et al., 2020), loss of confidence in such markets (Daehler et al., 2021), and significant reductions in international trade (Ramelli & Wagner, 2020).

It is important to note that although the disease caused by the SARS-CoV-2 virus affected all countries worldwide, its manifestations were more significant and pernicious in those considered emerging (Cakmakli et al., 2020). Moreover, such harmful effects are seen to a greater extent in Latin American economies with a greater predisposition or exposure to shocks originating in foreign markets (De Salles, 2021). Finally, regarding the research topic, empirical evidence indicates that during the pandemic, financial managers chose to increase cash holdings as a measure to cushion uncertainty (Xiuhong et al., 2020; Tomohito & Lichiro, 2021; Hoang et al., 2022). Even companies operating in the sectors most affected by the pandemic, which therefore faced larger cash shortfalls during that period, may have pressures on their cash flows in the long term (Xiuhong et al., 2020).

Methodological aspects

Financial information was obtained from the Economática database; closing prices for calculating stock returns were obtained from Investing. The sample analyzed comprises 29 non-financial companies listed on the Mexican Stock Exchange (BMV). Table 1 lists the issuers and their ticker symbol, highlighting the sector of economic activity to which they belong and the percentage they represent within the sample. The analysis period is from Q1 2001 to Q1 2022.

Table 1 Companies included in the sample

| Sector | Company | Code |

|---|---|---|

| Frequently consumed products N =7 24% |

Industrias Bachoco, S.A.B. de C.V. Grupo Bimbo, S.A.B. de C.V. Coca-Cola Femsa, S.A.B. de C.V. Gruma, S.A.B. de C.V. Kimberly - Clark de México S.A.B. de C.V. Organización Soriana, S.A.B. de C.V. Wal-Mart de México, S.A.B. de C.V. |

BACHOCO BIMBO KOF GRUMA KIMBER SORIANA WALMEX |

| Materials N =10 35% |

Grupo Pochteca, S.A.B. de C.V. Cemex, S.A.B. de C.V. Corporación Moctezuma, S.A.B. de C.V. Cydsa, S.A.B. de C.V Fomento Económico Mexicano, S.A.B. de C.V. Grupo Simec, S.A.B. de C.V. Industrias Ch, S.A.B. de C.V. Industrias Peñoles, S. A.B. de C. V. Grupo Lamosa, S.A.B. de C.V. Vitro, S.A.B. de C.V. |

POCHTEC CEMEX CMOCTEZ CYDSASA FEMSA SIMEC ICH PEÑOLES LAMOSA VITRO |

| Industrial N = 7 24% |

Alfa, S.A.B. de C.V. Consorcio Ara, S.A. de C.V. Grupo Aeroportuario del Sureste, S.A.B. de C.V. Grupo Carso, S.A.B. De C.V. Grupo Industrial Saltillo, S.A.B. De C.V. Grupo Kuo, S.A.B. De C.V. Orbia Advance Corporation, S.A.B. De C.V. |

ALFA ARA ASUR GCARSO GISSA KUO ORBIA-MEXICHEM |

| Services and non-basic consumer goods N = 2 7% |

Alsea, S.A.B. De C.V. Grupo Elektra, S.A.B. De C.V. |

ALSEA ELEKTRA |

| Telecommunication services N= 3 10% |

América Móvil, S.A.B. De C.V. Grupo Televisa, S.A.B. TV Azteca, S.A.B. De C.V. |

AMX TLEVISA AZTECA |

Source: created by the authors.

Considering the methodology proposed by Opler et al. (1999), one of the first efforts to address the determinants of cash levels based on endogenous business factors, the present study includes the variables company size, growth opportunities, leverage, cash flow, capital expenditure, cash substitution, cash flow risk, and dividends.

Size indicates the maturity and stability of organizations; young companies can use cash as a source of financing for growth, so larger companies tend to require lower cash levels.

Growth opportunities are operationalized by the ratio of market to book value; a small value indicates few investment opportunities, in which case there are incentives for managers to use cash with discretion.

Companies with access to external financing tend to maintain lower cash levels, as they can obtain the necessary resources from the financial system.

Cash flow determines the ability to generate profits from operations, so a positive association with cash levels would be expected.

Capital expenditure represents investments in fixed assets, so a negative association with cash levels is expected.

Cash substitution describes the ability to generate cash by converting current assets, so companies with higher current assets tend to hold lower cash levels.

According to the precautionary motive, cash can offset the effects of uncertainty; a company with high revenue volatility may use cash as a risk buffer.

Dividend payments reduce available liquid resources, so an inverse relation between dividend payments and cash levels is expected.

In order to include in the specification, the effect of financial managers’ decisions in light of market behavior, the return of the BMV’s Price and Quotations Index (PQI) is introduced into the analysis. Another variable that is integrated into the analysis is Mexico’s EMBI3, since in addition to considering risk from the perspective of international capital, an aspect strongly related to cash levels (Dittmar et al., 2003; Hardford et al., 2008; Huang et al., 2013; Iskandar & Jia, 2014), it also enables representing, to a certain extent, elements associated with domestic systematic risk (López et al., 2013). In order to adjust the data to obtain the parameters for panel data, it was decided to calculate the correlation coefficient between the returns of both indicators (PQI and EMBI) and the respective stock returns of the issuers in the sample. Table 2 provides important information on the variables used.

Table 2 Study variables

| Variable | Code | Operationalization |

|---|---|---|

| Cash level | cash |

|

| Country risk | embi |

|

| Market risk | pqi |

|

| Growth opportunities | action |

|

| Company size | size | natural logarithm of total assets |

| Cash flow | flow |

|

| Cash substitution | substitution |

|

| Capital expenditures | capex |

|

| Leverage | lever |

|

| Cash flow risk | risk | standard derivation |

| Dividends | dividends | dummy variable with a value of 1 for periods when dividends are paid and 0 for periods when dividends are not paid |

| Covid-19 | covid | dummy variable with a value of 1 from Q2 2020 onwards, 0 for the other periods |

*

Source: created by the authors.

The panel data methodology analyzes how the cash level responds to the proposed explanatory determinants, capturing unobservable heterogeneity over time and across cross-sectional units. This technique makes it possible to characterize at the same time two fundamental aspects of the unobservable process that generates the data: individual and temporal effects. The general linear regression model for panel data used to obtain the parameters that establish the relation between the behavior of the cash levels of the 29 issuers in the sample and the proposed series of proposed determinants can be seen in Equation 1.

Where

Given the unobservable differences in the financial policies of the issuers in the sample, it is easy to assume a heterogeneous component in their behavior, which would trigger the presence of relevant biases in the model presented in Equation 1. To reduce the random perturbation attributable to the issuer, and under the assumption that this effect is non-random, an intercept for each cross-sectional unit can be included in the specification, that is, an individual or specific effect, which results in a model with fixed effects:

On the other hand, if the individual effect is considered to be random, the white noise term should reflect the following:

Empirical analysis

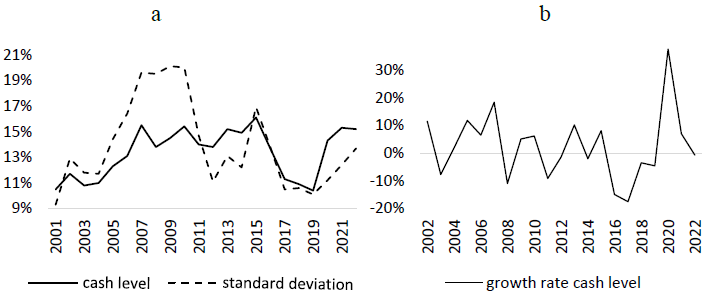

Panel (a) of Figure 1 shows the overall average and standard deviation of the cash level of the issuers under study. As can be seen, the cash level has witnessed a remarkable increase (44.8%) from 10.5% in 2001 to 15.2% in 2022, a situation that is consistent with previous studies (Xiuhong et al., 2020; Honda & Uesugi, 2021; Hoang et al., 2022). During this period, 83% of the issuers increased their cash level, which could be explained, at least in part, by the uncertainty in the financial markets due to the COVID-19 pandemic. Another important aspect of Figure 1 is the volatility of cash; the indicator corresponding to the standard deviation was higher between 2007 and 2010, a period that coincides with the subprime mortgage crisis; it is striking that at the beginning of the pandemic, the indicator was more stable than in other periods of uncertainty. Panel (b) of Figure 1 shows the rate of change of the cash level, whose dynamics remain more or less constant from the beginning of the series until the end of 2019, after which, coinciding with the pandemic by COVID-19, the indicator shoots up significantly.

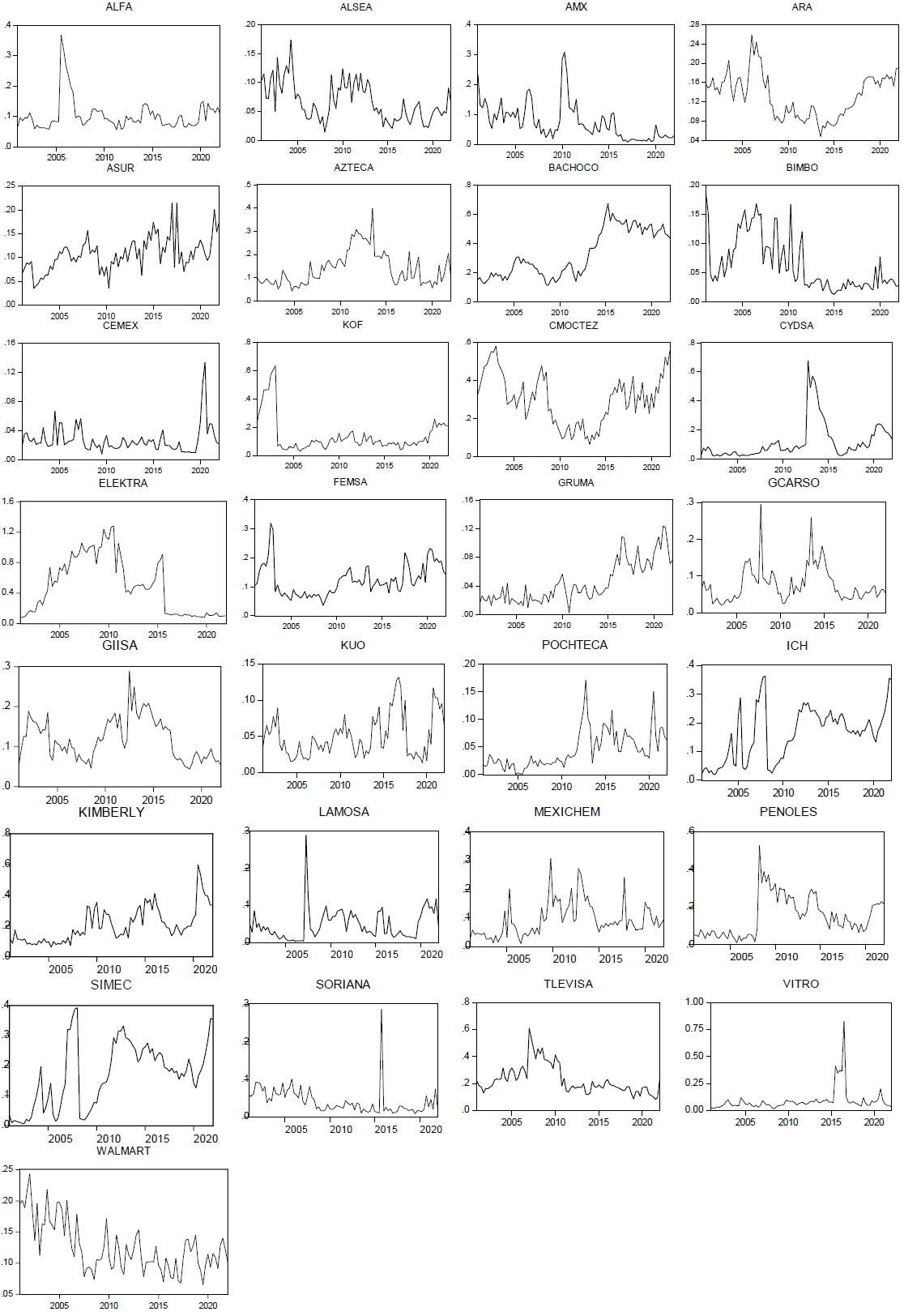

Figure 2 shows the cash level of some issuers, showing a heterogeneous behavior over time, especially toward the end of the period when the COVID-19 pandemic was declared. The greatest contrasts are perceived in ARA, ASUR, KOF, CMOCTEZ, ELEKTRA, FEMSA, GRUMA, GCARSO, GIISA, ICH, KIMBERLY, and SIMEC.

First, an evaluation is made of whether there are changes in the cash level of issuers before and after Q2 2020, when the capital markets reflected the effects of the COVID-19 pandemic. The information in Table 3 confirms statistically relevant changes in the cash level of issuers; the values enable the rejection of the null hypothesis of equality of means at a high level of significance. Since the t-test was conducted only in the periods adjacent to the COVID-19 pandemic declaration, it would be expected that the null hypothesis would be rejected in more cases if the test horizon were extended, as suggested by the behavior by issuer in Figure 2.

Table 3 Tests of difference in means

| Issuer | μ1 | μ2 | Est. t | P-value |

|---|---|---|---|---|

| ALFA | .0801 | .1219 | -3.3023 | .0131** |

| ALSEA | .0398 | .0572 | -2.4270 | .0456* |

| ASUR | .1049 | .1379 | -3.2370 | .0143* |

| KOF | .1050 | .2158 | -7.9925 | .0001*** |

| CMOCTEZ | .2976 | .4216 | -3.6758 | .0079*** |

| CYDSA | .1106 | .1991 | -3.7863 | .0068*** |

| GRUMA | .0735 | .0985 | -2.9772 | .0206** |

| GCARSO | .0507 | .0593 | -3.3369 | .0125** |

| KUO | .0226 | .0840 | -7.0461 | .0002*** |

| POCHTECA | .0426 | .0824 | -3.9380 | .0060*** |

| KIMBERLY | .1903 | .4140 | -4.7256 | .0021*** |

| LAMOSA | .0264 | .0929 | -4.7909 | .0020*** |

| PENOLES | .0912 | .1950 | -5.4919 | .0009*** |

*, **, *** indicates statistical significance at 95%, 99%, and <99% confidence level, respectively

Source: created by the authors.

Table 4 shows the descriptive statistics of the variables used.

Table 4 Average values, in annual terms

| Year | cash 10% | cash σ | embi | pqi | action | size* | flow | sust** | capex | lever | risk |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2001 | 0.105 | 0.093 | -0.30 | 0.32 | 1.73 | 55 573 | 6.4 | 4.1 | 0.58 | 0.47 | 0.039 |

| 2002 | 0.117 | 0.129 | -0.25 | 0.33 | 1.57 | 57 110 | 6.1 | 4.7 | 0.83 | 0.47 | 0.037 |

| 2003 | 0.108 | 0.118 | -0.31 | 0.30 | 1.06 | 63 818 | 5.5 | 3.9 | 0.95 | 0.48 | 0.035 |

| 2004 | 0.110 | 0.117 | -0.32 | 0.33 | 1.42 | 69 657 | 6.5 | 5.0 | 0.77 | 0.49 | 0.033 |

| 2005 | 0.123 | 0.144 | -0.32 | 0.38 | 1.79 | 79 492 | 7.0 | 5.4 | 0.76 | 0.48 | 0.034 |

| 2006 | 0.131 | 0.164 | -0.27 | 0.43 | 1.99 | 87 530 | 7.5 | 5.0 | 0.93 | 0.47 | 0.035 |

| 2007 | 0.155 | 0.196 | -0.34 | 0.47 | 2.75 | 102 419 | 7.1 | 4.9 | 1.42 | 0.47 | 0.037 |

| 2008 | 0.138 | 0.195 | -0.23 | 0.46 | 2.46 | 112 247 | 6.0 | 3.6 | 1.00 | 0.51 | 0.038 |

| 2009 | 0.145 | 0.201 | -0.29 | 0.46 | 2.31 | 127 310 | 5.5 | -0.3 | 0.03 | 0.54 | 0.041 |

| 2010 | 0.154 | 0.200 | -0.29 | 0.39 | 2.67 | 130 607 | 5.9 | 3.6 | -0.43 | 0.52 | 0.039 |

| 2011 | 0.140 | 0.147 | -0.32 | 0.43 | 2.74 | 142 823 | 6.2 | 6.0 | 1.04 | 0.51 | 0.035 |

| 2012 | 0.138 | 0.111 | -0.29 | 0.30 | 3.04 | 147 530 | 6.7 | 7.8 | 0.30 | 0.50 | 0.034 |

| 2013 | 0.152 | 0.131 | -0.28 | 0.38 | 3.35 | 149 052 | 5.8 | 6.0 | 0.86 | 0.50 | 0.040 |

| 2014 | 0.149 | 0.122 | -0.26 | 0.37 | 3.24 | 160 122 | 5.1 | 4.9 | 0.87 | 0.51 | 0.040 |

| 2015 | 0.161 | 0.169 | -0.37 | 0.37 | 3.26 | 172 347 | 5.6 | 4.1 | 0.47 | 0.52 | 0.039 |

| 2016 | 0.137 | 0.138 | -0.26 | 0.36 | 3.37 | 192 259 | 6.0 | 4.4 | 1.82 | 0.53 | 0.030 |

| 2017 | 0.113 | 0.105 | -0.27 | 0.28 | 3.27 | 187 559 | 5.5 | 3.8 | 0.28 | 0.54 | 0.028 |

| 2018 | 0.109 | 0.106 | -0.17 | 0.39 | 3.02 | 186 511 | 5.4 | 3.6 | 0.53 | 0.55 | 0.029 |

| 2019 | 0.104 | 0.101 | -0.29 | 0.31 | 2.78 | 194 284 | 4.7 | 2.0 | -0.07 | 0.56 | 0.029 |

| 2020 | 0.143 | 0.112 | -0.30 | 0.35 | 2.81 | 206 634 | 4.6 | 1.1 | 0.16 | 0.59 | 0.028 |

| 2021 | 0.153 | 0.124 | -0.29 | 0.27 | 3.52 | 191 236 | 7.1 | 0.4 | 0.15 | 0.57 | 0.032 |

| 2022 | 0.152 | 0.137 | -0.31 | 0.32 | 4.37 | 188 080 | 3.0 | 1.2 | -0.05 | 0.57 | 0.037 |

* Figures in millions of pesos, but the analysis uses the logarithm of assets; ** Sust refers to the substitution effect

Source: created by the authors.

The embi values are negative, which implies an inverse correlation with the issuers’ stock market performance. Even at the individual level, there are negative correlations in all cases. On the other hand, pqi shows a positive correlation but with a negative trend. The trend of both variables brings the correlation value close to zero, so the linear association has weakened during the study period.

The share variable shows an overall average of 2.66 times with a clear upward trend, perceived as an increase in investor confidence in the issuers’ performance in the future. Regarding size, Table 4 shows that the value of assets rose from MXN 55 573 000 000 in 2001 to MXN 188 080 000 000 in 2021, which implies a growth rate of 5.9% per year. It should be noted that during the years 2021 and 2022, the companies presented a contraction in total assets. In general, there is a significant dispersion in this category; the case of AMX could exemplify such a statement: by 2022, the company had 2.3 times the assets of the second largest company in the sample (FEMSA) and 293.6 times more than the company with the least assets in the sample (POCHTEC).

The flow variable remains relatively stable during the period analyzed, with an average value of 6.0%. Notably, this variable shows a negative trend over time, implying that issuers tend to generate lower profitability in their operations. The average quarterly flow value (for the entire period) was 2.5%, 4.9%, 7.3%, and 9.4% for Q1, Q2, Q3, and Q4, respectively, considering the accumulated annual earnings. In the first half of 2020, the lowest levels of the variable were observed: 1.9% in Q1 and 3.1% in Q2. The companies classified as frequent consumption and materials obtained, as a whole, a flow of 6.4% in the period from 2020 to 2022; in contrast, the companies identified as industrial, services, and non-basic consumer goods, as well as telecommunications services, obtained a flow of 2.8% for the same period. On the other hand, the risk has an overall average of 0.035, and although the series shows a negative trend, it is worth noting its stability over time.

The observed substitution averaged 4% and showed a negative trend. In addition, a significant drop was observed during the 2008 mortgage crisis, when the variable registered its lowest level (-0.3% during 2009). In 2012 the variable registered its best level (7.74%), after which it decreased to 0.4% during 2021, although it showed a slight recovery during 2022.

The capex ratio averages 0.6% and presents the lowest levels during the 2009-2010 and 2019-2022 periods, which coincides with the subprime crisis and the Covid-19 pandemic, respectively; this situation implies that Mexican companies reduced total investment in fixed assets during these events. The level of leverage shows an increasing trend from 2001 to 2020, when it reaches its historical maximum (58.5%), to drop to 56.7% in 2022. In aggregate terms, the periods with the greatest increase compared to the previous year are 2008, 2009, and 2020, with a rate of change of 7.1%, 5.3%, and 4.0%, respectively. Finally, the behavior of the number of issuers that pay dividends also shows a negative trend; it is noteworthy that during 2020 and 2021, the percentage of issuers that paid dividends was 55.2% and 62.1%, respectively.

In order to avoid obtaining results from spurious relations, the null hypothesis of the presence of a unit root was tested considering the longitudinal structure of the data. Table 5 demonstrates stationarity in common unit root processes (Levin, Lin, and Chu test) and individual processes (Im, Pesaran, and Shin, augmented Dickey-Fuller, and Phillips-Perron tests). Table 5 shows stationarity for all variables, except for risk, where the presence of unit root cannot be rejected under any test.

Table 5 Unit root tests

| Joint processes | Individual processes | |||

|---|---|---|---|---|

| Variable | LLCi | IPSii | ADFiii | PPiv |

| capex | -9.996*** | -19.911*** | 497.288*** | 808.714*** |

| dividends | -12.034*** | -21.580*** | 479.901*** | 692.817*** |

| cash | -2.230** | -5.565*** | 125.344*** | 274.457*** |

| embi | -8.279*** | -16.548*** | 393.033*** | 900.119*** |

| flow | -8.043*** | -17.993*** | 379.450*** | 754.444*** |

| mtob | -2.456*** | -3.685*** | 105.535*** | 141.992*** |

| lever | -0.660 | -1.150 | 67.897 | 115.798*** |

| pqi | -6.951*** | -11.305*** | 254.698*** | 721.946*** |

| risk | -0.280 | 0.165 | 60.811 | 54.907 |

| substitution | -2.156** | -5.742*** | 141.321*** | 270.905*** |

| size | -4.615*** | -0.089 | 69.483 | 77.178* |

i Levin, Lin and Chu (t), ii Im, Pesaran and Shin (w), iii Augmented Dickey-Fuller (Fisher X2), iv Phillips-Perron (Fisher X2). *, **, *** indicates statistical significance at 95%, 99% and < 99% confidence level, respectively

Source: created by the authors.

Nevertheless, the rejection of the presence of unit roots would lead to expecting significant differences in the probability distribution of the series under analysis. The information in Table 6 demonstrates such differences in the first two moments of the distribution.

Table 6 Tests for differences in mean and variance

| μ | σ | ||||

|---|---|---|---|---|---|

| Anova F-test | Welch F-test* | Bartlett | Levene | Brown-Forsythe | |

| cash | 76.66*** | 86.03*** | 2364.99*** | 83.07*** | 64.09*** |

| embi | 3.14*** | 3.097*** | 36.43 | 1.73 | 1.44 |

| pqi | 85.63*** | 106.46*** | 146.39*** | 5.32*** | 4.78*** |

| share | 1.31 | 60.58*** | 15545.19*** | 4.78*** | 1.28 |

| size | 500.20*** | 1110.86*** | 1643.85*** | 68.74*** | 38.59*** |

| flow | 38.97*** | 26.58*** | 601.54*** | 17.13*** | 13.66*** |

| substitution | 219.87*** | 360.02*** | 1525.53*** | 24.79*** | 18.75*** |

| capex | 2.01*** | 6.11*** | 1405.67*** | 5.66*** | 5.29*** |

| lever | 263.50*** | 810.10*** | 943.31*** | 37.17*** | 27.69*** |

| risk | 50.64*** | 195.64*** | 2273.71*** | 46.74*** | 23.67*** |

*, **, *** indicates statistical significance at 95%, 99% and <99% confidence level, respectively

Source: created by the authors.

Once the existence of significant differences in mean and variance in the information analyzed was demonstrated, Equation 1 was used to estimate the response of the cash level to the explanatory factors proposed in this study, using the following specification:

Where subscript i refers to the i—th issuer in the sample, subscript t captures the period, and

Under a pooled model, the first estimations reveal that only the flow, leverage, risk, and substitution variables have a relevant effect on the cash level. Nevertheless, despite the high statistical significance of the parameters, the coefficients of the LR test show that the residuals of the regression are heteroskedastic, and therefore, the pooled model is not appropriate, as shown in Table 7.

Table 7 LR test of heteroskedasticity for panel data

*, **, *** indicates statistical significance at 95%, 99% and <99% confidence level, respectively

Source: created by the authors.

The next step was estimating the fixed effects model in Equation 2. Although the fixed effects redundancy tests showed coefficients and significance levels that enable the rejection of the null hypothesis that such effects are redundant (81.295 and 0.00 for the F-test coefficient and its respective p-value, and similarly 1 624.644 and 0. 00 in the case of the X2 test), the random effects model was estimated from Equation 3. In order to capture the effect of the Covid-19 pandemic on the specification in Equation 4, the regression parameters were obtained by dividing the study horizon into three periods, that is, i) taking the entire horizon, ii) from the beginning until the declaration of the pandemic and iii) from Q2 2020to the end of the analysis period. The results are shown in Table 8.

Table 8 Estimation results by sub-periods

| (A) | ||||||

| Q12001-Q12022 | Q12001-Q12020 | Q22020-Q12022 | ||||

| Variable | Coef. | P-value | Coef. | P-value | Coef. | P-value |

| intercept | 0.015 | 0.846 | 0.016 | 0.845 | -0.084 | 0.730 |

| share | -5.76E-05 | 0.257 | -7.01E-05 | 0.165 | -1.16E-04 | 0.438 |

| capex | -0.048 | 0.441 | -0.022 | 0.726 | 0.006 | 0.351 |

| embi | 0.002 | 0.716 | 1.25E-04 | 0.98 | 0.022 | 0.317 |

| pqi | 0.072 | 0.000*** | 0.074 | 0.000*** | -0.006 | 0.264 |

| dividends | -0.018 | 0.000*** | -0.016 | 0.003*** | 0.217 | 0.463 |

| flow | 0.328 | 0.000*** | 0.257 | 0.000*** | 8.00E-04 | 0.001*** |

| lever | -0.244 | 0.000*** | -0.299 | 0.000*** | -0.131 | 0.071 |

| risk | 0.623 | 0.000*** | 0.653 | 0.000*** | 1.965 | 0.000*** |

| substitution | -0.319 | 0.000*** | -0.362 | 0.000*** | -0.087 | 0.076 |

| size | 0.011 | 0.012** | 0.013 | 0.006*** | 0.013 | 0.348 |

| (B) | ||||||

| Hausman X2 Test | ||||||

| Q12021-Q12022 | Q12021-Q12020 | Q22020-Q12022 | ||||

| coefficient | 11.358 | 11.670 | 38.766 | |||

| p-value | 0.330 | 0.308 | 0.000*** | |||

*, **, *** indicates statistical significance at 95%, 99% and <99% confidence level, respectively

Source: created by the authors.

The first two columns in Table 8 offer the result of the base estimates for the entire time horizon of the study, i.e., from Q1 2001 to Q1 2022. The first noteworthy result is that the cash levels of the issuers in the sample respond significantly to pqi, dividends, flow, leverage, risk, substitution, and size. The dependent variable responds negatively to substitution, leverage, and dividends, in order of importance regarding the magnitude of the effect (share and capex also show an inverse effect on cash levels). On the other hand, the variables risk, flow, pqi, and size directly affect the dependent variable.

Another important aspect of the information contained in Table 8 is that when comparing the estimates for the full period (from Q1 2001 to Q1 2022) against those for the period Q1 2001-Q1 2020, the information shows that the response of the cash level to the proposed explanatory factors is maintained, in terms of its high level of significance and the sense of the relation. On the other hand, the response of the cash level is different in the pre-pandemic period versus the full period: the effect of the independent variables is higher for pqi, leverage, risk, substitution, and size, i.e., the effect of the pandemic decreased the relative importance of the explanatory factors. In contrast, the impact on the dependent variable from the pandemic declaration was lower for dividends and flow.

Such results are an indicator that the level of cash in the sample issuers is influenced by the precautionary motive, given that cash can be used as a buffer against increased cash flow volatility (Opler et al., 1999; Almeida et al., 2004; Bates et al., 2009; Sun & Wang, 2015), as happens in periods of instability such as the one following the global pandemic. In order to exemplify the above, evidence shows that during the pandemic period, companies increased their debt levels, contracted fixed asset investments, and reduced dividends, presumably to protect liquidity in the face of declining flows and the increased volatility of the latter.

Regarding the estimates in the period after the pandemic declaration, which is observed in the last column of Table 8, it can be seen that only cash flow and risk are statistically relevant in explaining the behavior of the cash level, in both cases maintaining the direct relation shown in the two previous groups. A tentative explanation for this behavior is that, faced with the volatility generated by the pandemic, the companies modified their financial structure and increased their cash holdings as a shield against uncertainty, whereby the companies, following the precautionary motive, increased cash to protect their operations from the uncertainty generated.

Finally, it is important to note that comparing the fixed and random effects models is conventionally based on the Hausman test, which evaluates the null hypothesis of systematic differences between the estimators obtained by both models. For the three periods, the X2 value of the Hausman test, shown in panel (B) of Table 8, suggests that it is more convenient to use the more efficient model versus the more consistent one, i.e., the random effects model is better than the fixed effects model. The test result is consistent with the expected result and is posed in Equation 3. Under the random effects approach,

With the intention of explicitly including the effect of the COVID-19 pandemic in the specification proposed in Equation 4, a dummy variable is included that acquires the value of one from the second quarter of 2020, when the WHO health authorities officially declared the pandemic, and zero in any other case, considering the entire study period, that is, from Q1 2001 to Q1 2022. The results are shown in Table 9.

Table 9 Estimate results for the period Q1 2001- Q1 2022

| Variable | Coefficient | T-statistic | P-value |

|---|---|---|---|

| intercept | 0.070 | 0.876 | 0.381 |

| share | -7.01E-05 | -1.138 | 0.255 |

| capex | -0.034 | -0.543 | 0.587 |

| embi | 0.001 | 0.287 | 0.774 |

| pqi | 0.078 | 6.508 | 0.000*** |

| dividends | -0.014 | -2.601 | 0.009*** |

| flow | 0.300 | 5.598 | 0.000*** |

| lever | -0.250 | -9.408 | 0.000*** |

| risk | 0.642 | 5.312 | 0.000*** |

| substitution | -0.316 | -12.414 | 0.000*** |

| size | 0.008 | 1.748 | 0.081 |

| covid | 0.026 | 3.340 | 0.001*** |

| Hausman Testp X2 | 12.113 | 0.355 | |

*, **, *** indicates statistical significance at 95%, 99% and <99% confidence level, respectively

Source: created by the authors.

The information in Table 9 shows that the proposed factors maintain the sense and significant effect on the level of cash as shown in Table 8, except for the size variable which in the new estimation presents a p-value of 0.08. Likewise, the positive and highly significant effect of the COVID-19 pandemic on the cash level of the issuers in the sample is confirmed, suggesting that the health crisis was a factor that encouraged the companies to maintain greater liquidity.

The pqi variable significantly explains the cash level, implying that a favorable performance of issuers in the stock markets favors the company’s ability to hold cash. On the other hand, the theory indicates that dividends maintain an inverse relation with cash, a result corroborated by the sample’s empirical data; the companies that decide to retain the company’s profits accumulate higher levels of cash. Notably, during the pandemic period, the number of companies that declared dividends decreased while cash reserves increased.

The negative relation of leverage with cash levels indicates that Mexican companies that can find resources in financial markets tend to hold less cash than those that may have difficulty accessing external resources. Other studies that find an inverse association are Acharya et al. (2007) and Harford et al. (2008).

The positive effect of cash flow is consistent with the results of Opler et al. (1999), who point out that the level of cash is associated with the company’s capacity to generate revenues. Likewise, the positive impact of risk on cash levels is as expected, in line with the precautionary motive pointed out by Keynes, so it could be assumed that there is a direct association between cash and risk since a company that has greater volatility in its cash flow will face greater difficulties in carrying out plans.

The inverse relation between substitution and the dependent variable implies that companies with more current assets are confident in their ability to generate short-run liquidity, thus requiring them to hold smaller amounts of cash.

Although theoretically one would expect larger companies to require lower levels of cash than smaller companies, the direct relation of the size variable shown in Table 9 is consistent with previous work (Chen & Chuang, 2009; Lee & Lee, 2009; Kuan et al., 2011; and Kusnadi, 2011). The positive relation between size and cash can be explained by the degree of information asymmetry in a country, such that protection for shareholders is weak so that managers can maintain discretion over cash (Weidemann, 2018).

Conclusions

Because of their influence on corporate financial performance, as well as their effect on the expectations of different economic agents, short-run financial decisions, particularly the level of cash that a company maintains in its financial structure, has been a topic of interest in the financial research agenda since Keynes’ explanations regarding the utility of money. This study provides empirical evidence of the effect of a series of proposed factors on the cash level of a group of issuers operating in the Mexican stock market. Using the panel data analysis technique, the observations of 29 issuers between Q1 2000 and Q2 2022 are analyzed, contrasting the effect of the COVID-19 pandemic relation mentioned above.

The analysis results contribute to several aspects of the financial literature on short-run decisions. First, and to the best of general knowledge, this is the first effort to analyze the behavior of the cash level of issuers listed on the Mexican Stock Exchange based on a group of explanatory factors. In general terms, the analysis conducted confirms the findings of similar studies conducted in other economies in the sense of evidence that the level of liquidity of the companies has been increasing significantly and that the largest increase, almost 70%, is perceived between 2019 and 2020, a period that corresponds to the detection of the SARS-COV-2 virus.

Secondly, the analysis documents a significant relation between the factors proposed as explanatory variables of the cash held in their financial structure by the companies studied. The relation with the level of cash is direct and in order of importance concerning the volatility of cash flows, how assets contribute to generating operating revenue, the correlation between stock market performance and the PQI, as well as the size of the company. The relation is inverse, and in order of importance to the substitution effect, the level of leverage, and dividends.

Finally, the results of the estimations show that the significance and sense of the explanatory relation of the proposed factors, which were appreciated in the period before the outbreak of the pandemic, were maintained once the pandemic was declared. Nevertheless, the change in the coefficients associated with such factors when considering the effect of the pandemic reveals that from the onset of the health crisis, cash flow, cash substitution, and leverage had a greater effect on the level of cash. On the other hand, the reaction of the dependent variable was smaller for dividends, the relation with the PQI, risk, and the company’s size.

The results could interest those interested in investment and financing policies, especially during unexpected economic and financial shocks. The analysis suggests that the sample issuers’ cash level is influenced, to some extent, by the precautionary motive defined by Keynes. Companies use liquidity as a buffer against increased volatility in internal cash flows and the relation to the market. It is worth noting that such a response is proportional to the size of the companies. As expected, the need for cash is inversely proportional to the liquidity of current assets. Notably, the level of leverage and shareholder commitments (dividends) reduce the need to hold cash.

It would be interesting to delve deeper into the differentiated effect of factors representing domestic systematic risk on the level of cash that companies decide to keep in their financial structure according to the sector of economic activity, type of ownership, and size of the companies, among other aspects. Likewise, it would be important to analyze how different shocks transmitted through financial markets impact short-run financial decisions, such as the level of cash. For the time being, this work will be deferred for future efforts.

REFERENCES

Acharya, V. V., Almeida, H., y Campello, M. (2007). Is cash negative debt? A hedging perspective on corporate financial policies. Journal of Financial Intermediation, 16(4), 515-554. https://doi.org/10.1016/j.jfi.2007.04.001. [ Links ]

Almeida, H., Campello, M., y Weisbach, M. S. (2004). The cash flow sensitivity of cash. The Journal of Finance, 59(4), 1777-1804. https://doi.org/10.1111/j.1540-6261.2004.00679.x. [ Links ]

Ali, M., Alam, N., y Rizvi, S. (2020). Coronavirus (Covid-19)- An epidemic or pandemic for financial markets. Journal of Behavioral and Experimental Finance, 27, 1-6. https://doi.org/10.1016/j.jbef.2020.100341. [ Links ]

Arellano, M., y Bover, O. (1995). Another look at the instrumental variable estimation of error-components models. Journal of econometrics, 68(1), 29-51. https://doi.org/10.1016/0304-4076(94)01642-D. [ Links ]

Bates, T. W., Kahle, K. M., y Stulz, R. M. (2009). Why do U.S. firms hold so much more cash than they used to? The Journal of Finance , 64(5), 1985-2021. https://doi.org/10.1111/j.1540-6261.2009.01492.x. [ Links ]

Baum, Caglayan, Ozkan y Talavera (2006). The impact of macroeconomic uncertainty on non-financial firms’ demand for liquidity. Review of Financial Economics, 15(4), 289-304. https://doi.org/10.1016/j.rfe.2006.01.002. [ Links ]

Baumol, W. J. (1952). The transactions demand for cash: An inventory theoretic approach. The Quarterly Journal of Economics, 66(4), 545-556. https://doi.org/10.2307/1882104. [ Links ]

Baker, S. R., Bloom, N., Davis, S. J., y Terry, S. J. (2020). Covid-induced economic uncertainty. National Bureau of Economic Research, working paper series, No. w26983. https://doi.org/10.3386/w26983. [ Links ]

Bibow, J. (1995). Some reflections on Keynes's ‘finance motive’ for the demand for money. Cambridge Journal of Economics, 19(5), 647-666. https://www.jstor.org/stable/23600187. [ Links ]

Bigelli, M., y Sánchez-Vidal, J. (2012). Cash holdings in private firms. Journal of Banking & Finance, 36(1), 26-35. https://doi.org/10.1016/j.jbankfin.2011.06.004. [ Links ]

Brandon, J., y Youngsuk, Y. (2012). Political uncertainty and corporate investment cycles. The Journal of Finance , 67(1), 45- 83. https://doi.org/10.1111/j.1540-6261.2011.01707.x. [ Links ]

Cakmakli, C., Demiralp, S., Ozcan, S. K., Yesiltas, S., y Yildirim, M. (2020). COVID-19 and emerging markets: an epidemiological model with international production networks and capital flows. IMF Working Paper No. 20/133. Disponible en https://ssrn.com/abstract=3670613. [ Links ]

Chen, Y. R., y Chuang, W. T. (2009). Alignment or entrenchment? Corporate governance and cash holdings in growing firms. Journal of Business Research, 62(11), 1200-1206. https://doi.org/10.1016/j.jbusres.2008.06.004. [ Links ]

Daehler, T., Aizenman, J., y Jinjarak, Y. (2021). Emerging markets sovereign CDS spreads during Covid-19: Economics versus epidemiology news. Economic Modelling, 100(105504). https://doi.org/10.1016/j.econmod.2021.105504. [ Links ]

De Salles, A. (2021). Covid-19 pandemic initial effects on the idiosyncratic risk in Latin America. Revista Mexicana de Economía y Finanzas, 16(3), 1-21. https://doi.org/10.21919/remef.v16i3.632. [ Links ]

D’Mello, R., Krishnaswami, S., y Larkin, P. J. (2008). Determinants of corporate cash holdings: Evidence from spin-offs. Journal of Banking & Finance , 32(7), 1209-1220. https://doi.org/10.1016/j.jbankfin.2007.10.005. [ Links ]

Dittmar, A., Mahrt-Smith, J., y Servaes, H. (2003). International corporate governance and corporate cash holdings. Journal of Financial and Quantitative analysis, 38(1), 111-133. https://doi.org/10.2307/4126766. [ Links ]

Duchin, R. (2010). Cash holdings and corporate diversification. The Journal of Finance , 65(3), 955-992. https://www.jstor.org/stable/25656318. [ Links ]

Ferreira, M. A., y Vilela, A. S. (2004). Why do firms hold cash? Evidence from EMU countries. European Financial Management, 10(2), 295-319. https://doi.org/10.1111/j.1354-7798.2004.00251.x. [ Links ]

Foley, C. F., Hartzell, J. C., Titman, S., y Twite, G. (2007). Why do firms hold so much cash? A tax-based explanation. Journal of financial economics, 86(3), 579-607. https://doi.org/10.1016/j.jfineco.2006.11.006. [ Links ]

Harford, J., Mikkelson, W., y Partch, M. M. (2003). The effect of cash reserves on corporate investment and performance in industry downturns. Working paper. [ Links ]

Harford, J., Mansi, S. A., y Maxwell, W. F. (2008). Corporate governance and firm cash holdings in the US. Journal of financial economics , 87, 535-555. https://doi.org/10.1016/j.jfineco.2007.04.002. [ Links ]

Hoang K., Cuong N., Dung V., y Anh P. (2022). International corporate cash holdings and firm-level exposure to COVID-19: Do cultural dimensions matter? Journal of Risk and Financial Management 15(262), pp. . https://doi.org/10.3390/jrfm15060262. [ Links ]

Honda C., y Uesugi I. (2021). COVID-19 and precautionary corporate cash holdings: evidence from Japan. RCESR Discussion Paper Series DP21-2, Research Center for Economic and Social Risks, Institute of Economic Research, Hitotsubashi University. https://ideas.repec.org/p/hit/rcesrs/dp21-2.html. [ Links ]

Huang, Y., Elkinawy, S., y Jain, P. K. (2013). Investor protection and cash holdings: Evidence from US cross-listing. Journal of Banking & Finance , 37(3), 937-951. https://doi.org/10.1016/j.jbankfin.2012.10.021. [ Links ]

Iskandar-Datta, M. E., y Jia, Y. (2014). Investor protection and corporate cash holdings around the world: new evidence. Review of Quantitative Finance and Accounting, 43(2), 245-273. https://doi.org/10.1007/s11156-013-0371-y. [ Links ]

Jensen, M. C., y Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of financial economics , 3(4), 305-360. https://doi.org/10.1016/0304-405X(76)90026-X. [ Links ]

Kaplan, S. N., y Zingales, L. (1997). Do investment-cash flow sensitivities provide useful measures of financing constraints? The Quarterly Journal of Economics , 112(1) 169-215. https://www.jstor.org/stable/2951280. [ Links ]

Keynes, J. M. (1936). The general theory of employment, interest, and money. Macmillan. [ Links ]

Kuan, T. H., Li, C. S., y Chu, S. H. (2011). Cash holdings and corporate governance in family-controlled firms. Journal of Business Research , 64(7), 757-764. https://doi.org/10.1016/j.jbusres.2010.07.004. [ Links ]

Kusnadi, Y. (2011). Do corporate governance mechanisms matter for cash holdings and firm value? Pacific-Basin Finance Journal, 19(5), 554-570. https://doi.org/10.1016/j.pacfin.2011.04.002. [ Links ]

Le, B. (2019). Working capital management and firm’s valuation, profitability and risk: Evidence from a developing market. International Journal of Managerial Finance, 15(2), 191-204. https://doi.org/10.1108/IJMF-01-2018-0012. [ Links ]

Lee, K. W., y Lee, C. F. (2009). Cash holdings, corporate governance structure and firm valuation. Review of Pacific Basin Financial Markets and Policies, 12(03), 475-508. https://doi.org/10.1142/S021909150900171X. [ Links ]

López, F. H., Venegas, F. M., y Gurrola, C. R. (2013). EMBI+ Mexico y su relación dinámica con otros factores de riesgo sistemático: 1997-2011. Estudios Económicos, 28(2) 193-216. https://estudioseconomicos.colmex.mx/index.php/economicos/article/view/81/83. [ Links ]

Luo, Q., y Hachiya, T. (2005). Corporate governance, cash holdings, and firm value: evidence from Japan. Review of Pacific Basin Financial Markets and Policies , 8(4), 613-636. https://doi.org/10.1142/S0219091505000580. [ Links ]

Martínez-Sola, C., García-Teruel, P. J., y Martínez-Solano, P. (2013). Corporate cash holding and firm value. Applied Economics Taylor & Francis, 45(2), 161-170. https://doi.org/10.1080/00036846.2011.595696. [ Links ]

Miller, M. H., y Orr, D. (1966). A model of the demand for money by firms. The Quarterly Journal of Economics , 80(3), 413-435. https://doi.org/10.2307/1880728. [ Links ]

Modigliani, F., y Miller, M. H. (1958). The cost of capital, corporation finance and the theory of investment. The American Economic Review, 48(3), 261-297. https://www.jstor.org/stable/1809766. [ Links ]

Myers, S. C., y Majluf, N. S. (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of financial economics , 13(2), 187-221. https://doi.org/10.1016/0304-405X(84)90023-0. [ Links ]

Opler, T., Pinkowitz, L., Stulz, R., y Williamson, R. (1999). The determinants and implications of corporate cash holdings. Journal of financial economics , 52(1), 3-46. https://doi.org/10.1016/S0304-405X(99)00003-3. [ Links ]

Ozkan, A., y Ozkan, N. (2004). Corporate cash holdings: An empirical investigation of UK companies. Journal of Banking & Finance , 28(9), 2103-2134. https://doi.org/10.1016/j.jbankfin.2003.08.003. [ Links ]

Palazzo (2012). Cash holdings, risk, and expected returns. Journal of financial economics , 104(1), 162-185. https://doi.org/10.1016/j.jfineco.2011.12.009. [ Links ]

Pinkowitz, L., y Williamson, R. (2002). What is a dollar worth? The market value of cash holdings. Working paper. https://ssrn.com/abstract=355840 or http://dx.doi.org/10.2139/ssrn.355840. [ Links ]

Pinkowitz, L., Stulz, R., y Williamson, R. (2006). Does the contribution of corporate cash holdings and dividends to firm value depend on governance? A cross‐country analysis. The Journal of Finance , 61(6), 2725-2751. https://doi.org/10.1111/j.1540-6261.2006.01003.x. [ Links ]

Ramelli, S., y Wagner, A. (2020). What the stock market tells us about the consequences of COVID-19; en Mitigating the COVID Economic Crisis: Act Fast and Do Whatever it Takes, Edited by Richard Baldwin and Beatrice Weder di Mauro; CEPR Press. [ Links ]

Sahai, A., Rath, N., Sood, V., & Singh, M. (2020). ARIMA modelling & forecasting of Covid-19 in top five affected countries. Diabetes & Metabolic Syndrome: Clinical Research & Reviews, 14(5), 1419-1427. https://doi.org/10.1016/j.dsx.2020.07.042. [ Links ]

Steijvers, T., y Niskanen, M. (2013). The determinants of cash holdings in private family firms. Accounting & Finance, 53(2), 537-560. https://doi.org/10.1111/j.1467-629X.2012.00467.x. [ Links ]

Sun, Z., y Wang, Y. (2014). Corporate precautory savings: Evidence from the recent financial crisis. The Quarterly Review of Economics and Finance, 56, pp. 175-186. https://doi.org/10.1016/j.qref.2014.09.006. [ Links ]

Tomohito, H., y Iichiro, U. (2021). COVID-19 and Precautionary corporate cash holdings: Evidence from Japan. RCESR Discussion Paper Series en https://ideas.repec.org/p/hit/rcesrs/dp21-2.html. [ Links ]

Weidemann, J. F. (2018). A state-of-the-art review of corporate cash holding research. Journal of Business Economics, 88, 765-797. https://doi.org/10.1007/s11573-017-0882-4. [ Links ]

Whalen, E. L. (1966). A Rationalization of the Precautionary Demand for Cash. The Quarterly Journal of Economics , 80(2), 314-324. https://doi.org/10.2307/1880695. [ Links ]

Xiuhong Q., Guoliang H., Huayu S., y Mengyao F. (2020). COVID-19 Pandemic and firm-level cash holding-moderating effect of goodwill and goodwill impairment. Emerging Markets Finance and Trade, 56(10), pp. 2243-2258. https://doi.org/10.1080/1540496X.2020.1785864. [ Links ]

Yepes, D. E., y Restrepo, T. D. (2016). Determinantes del nivel de efectivo de las compañías colombianas. Lecturas de economía, 85(julio- diciembre), 243-276. https://doi.org/10.17533/udea.le.n85a08. [ Links ]

Zhang, D., Hu, M., y Ji, Q. (2020). Financial markets under the global pandemic of COVID-19. Finance Research Letters, 36, en prensa, artículo no.101528. https://doi.org/10.1016/j.frl.2020.101528. [ Links ]

1 The average cash level of some issuers in the Mexican capital market increased from 10.5% in 2001 to 15.2% in 2022. More details are presented in the results section.

2 Thus, financial managers may choose to maintain cash levels above the optimal level and incur agency costs, in terms of Jensen and Meckling (1976).

Received: September 16, 2022; Accepted: November 25, 2022; Published: November 28, 2022

Este es un artículo publicado en acceso abierto bajo una licencia Creative Commons

Este es un artículo publicado en acceso abierto bajo una licencia Creative Commons